Investors in European equities are missing out if they just focus on listed stocks, particularly when it comes to the mid-cap sector.

Edmund Buckley Global Co-Head of Private Equity & Head of Direct Private Equity, Hugo Hickson Value Creation Principal Pictet Asset Managment.

Slowing economic growth, falling corporate earnings, high inflation. There are plenty of reasons for equity investors to be nervous. Yet there will always be investment opportunities even when economic conditions are tough. Some of them, we believe, can be found among privately-owned European small-and-mid-cap companies.

These are businesses that have already proven their potential, and are now looking to take the next step; to professionalise and grow. Private equity (PE) investors can help such firms make progress on this path by injecting new capital and – just as importantly – by providing strategic and operational expertise.

The investment opportunity is a large one. There are around 63,000 companies in Europe with revenues of EUR30-300 million.1 It’s also largely untapped – to date, only around 1.5 per cent of such companies in Europe receive PE investment per annum.2 The growth potential looks greater still when the US is the benchmark. Adjusted for GDP, small and mid-cap PE markets are four times larger in the US than in Europe.3

European companies were already becoming more open to PE involvement thanks to the emergence of a new generation of entrepreneurs (in France alone, investment in unlisted assets has tripled over the past three years).4 And as borrowing costs have risen and public markets have become harder and more costly to access, private companies have greater incentives to partner with PE managers.

But the expansion of Europe’s PE market isn’t the only attraction for investors looking to put their capital to good use.

Experience suggests that this particular phase of the economic cycle is especially favourable for private equity investments.

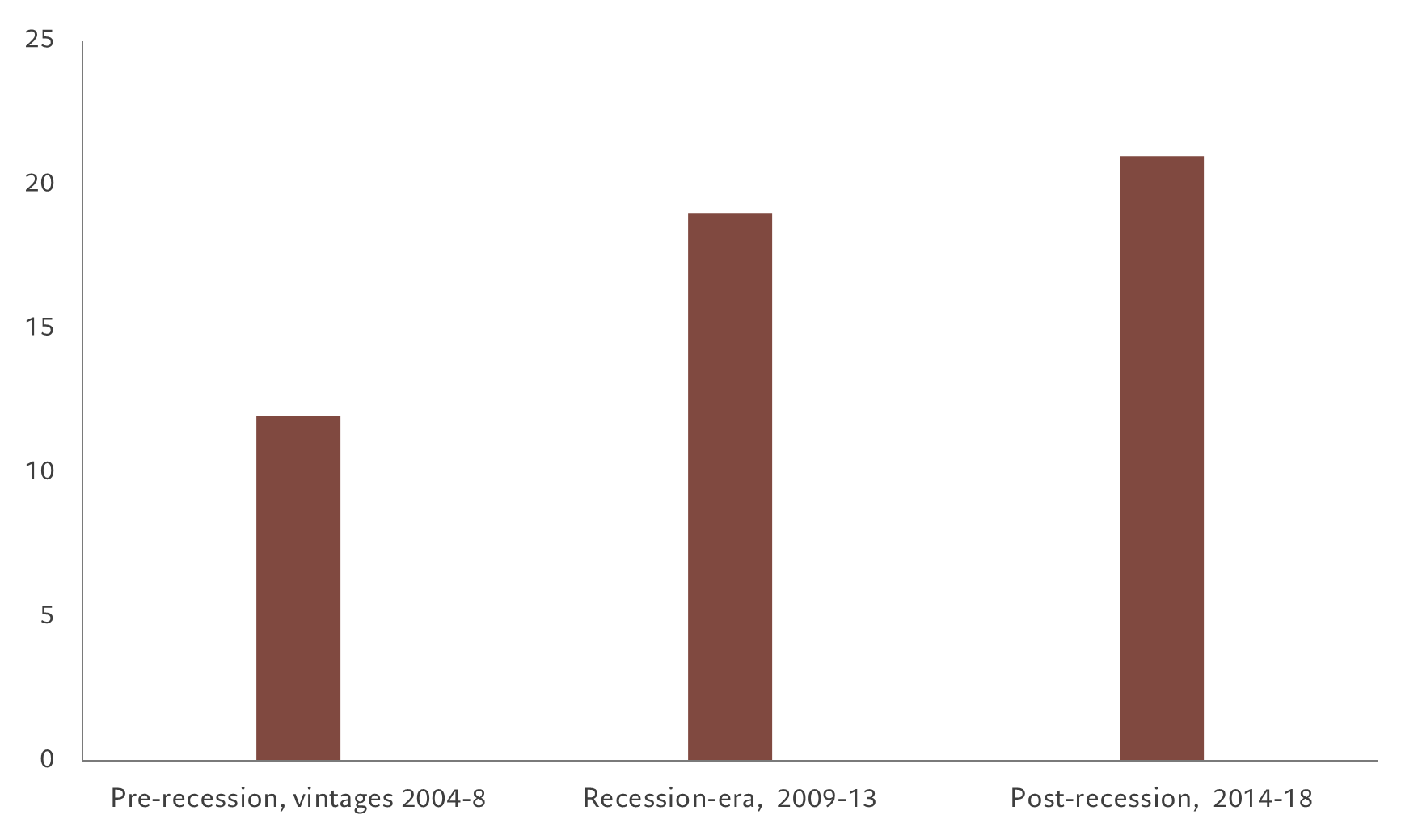

Historically PE fund vintages raised during, or immediately, after economic downturns have tended to be the best performers (see Fig 1). Within those, mid-market cap-focused strategies have done particularly well.5

Fig. 1 – Top performers

Performance of global private equity, gross IRR %

Source: McKinsey, “Global Private Markets Review”, 2022.

In such periods, allocating capital to mid-sized companies can pay off – and this is where direct PE funds may enjoy and advantage. That’s in part because tough macroeconomic conditions can create an attractive entry point for investment. But it is also because it is during such periods that bold and shrewd business management can really prove its worth – expertise that private equity managers can offer.

Embracing megatrends

In our view, many of Europe’s small-and-medium-sized, privately-owned companies operate sub-optimally. They often fail to fully harness operational efficiencies, and may lack a global presence, a strategic focus, and management resources. This is particularly the case when it comes to confronting some of the most pressing commercial challenges of our age, such as the digitisation of the economy or the clean energy transition.

Of course, these are problems that also face publicly listed companies. But in private markets, investors have the opportunity to be directly involved in engineering the necessary transformations.

The expansion of the digital world, for example, will have a major bearing on how companies operate, how they leverage data, how they segment customers and manage orders – all through the value chain. This can be a challenge for mid-sized companies, where resources are often focused on day-to-day running of the business, leaving limited energy and expertise to invest in new digital initiatives.

By end of 2019 only three in 10 European corporations had managed to significantly digitalise their business models.6 Although there has been some catch-up during Covid, a lot of work remains. Digital laggards need to speed up investment in tech – be that through creating mobile apps, entering the metaverse or embracing automation.

The clean energy transition is arguably even more urgent. The mitigation of climate change is already a priority for governments and regulators and increasingly so for consumers. Nearly half of the world’s very largest corporations have made Net Zero commitments, led by Europe (Germany and the UK in particular). A particularly thorny problem for small and medium cap companies is that regulators and investors are taking a much closer look at the corporate world’s carbon footprint. The steady adoption of Scope 3 emissions, a metric that aims to capture the carbon footprint of a company’s entire supply chain, will place a particularly heavy burden on Europe’s smaller and medium-sized firms for it is they that supply the materials to – and distribute the products of – the region’s largest firms.

But the clean energy transition will also bring opportunities for business expansion.

The sustainable economy will need software firms to run smart grids, for instance, and infrastructure companies to dig holes for cables carrying electricity from wind farms into cities. All in, decarbonising Europe’s energy system creates a USD5.3 trillion investment opportunity, according to BloombergNEF.7

Active partnership

As the breadth of European private investment opportunities expands, it would be tempting to allocate capital across a wide range of industries. But with economic conditions likely to be volatile for some time, we believe a wiser course would be to focus investments in sectors that can withstand the ups and downs of the business cycle.

These are industries that offer what we would describe as downside protection: sectors where spending continues even as the economy slows; where profit margins are attractive and resilient; and where there is good visibility on businesses’ future cash flows. Education and training is one such counter-cyclical sector, as people tend to spend more on education when labour markets are weaker.

In general, we believe the best way to manage risk and maximise returns is through active partnership with founders, families and entrepreneurial management teams of the businesses we invest in. By taking a majority stake in these small and middle-sized companies, and becoming a trusted partner of those firms, we can help transform good businesses into great ones.

To achieve that, it is also important to help the companies we invest in improve their environmental, social and governance (ESG) credentials. To us, that means focusing on environmental performance and improving the way in which a company manages its workforce, taking into account, among other things, the diversity of its leadership and employee engagement.

As well as creating value, the active approach also offers downside protection – by being more involved we are more likely to see any problems and have the chance to address them early.

[1] Capital IQ, 2022

[2] Invest Europe / EDC

[4] https://www.institutmontaigne.org/en/expressions/unlisted-investment-europes-untapped-potential

[5] McKinsey, “Global Private Markets Review”, 2022.

[6] IDC, 2019

[7] https://about.bnef.com/blog/europes-path-to-clean-energy-a-5-3-trillion-investment-opportunity/