Xiao Cui, Senior Economist – Pictet Wealth Management.

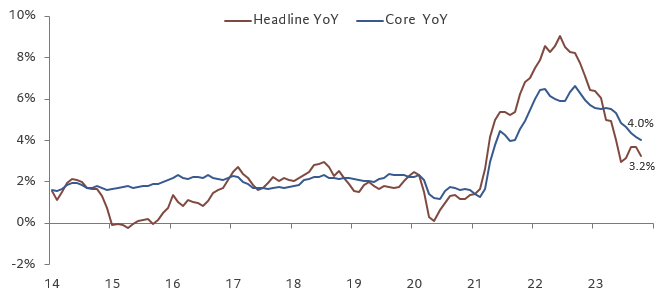

Core CPI came in weaker than consensus expectation, increasing 0.227% MoM (consensus: 0.3%). This is a step down from its 0.32% MoM print last month. The YoY reading fell further to 4.0% from 4.1%. Core inflation is headed in the right direction, as the 3m annualized growth rate is even lower at 3.4%.

Yesterday’s report is another step in the right direction in the Fed’s inflation fight, and should be welcome news for the FOMC. There will be another CPI and employment report before the December FOMC meeting, but yesterday’s downside surprise should further reduce the probability of another hike near term.

Policy bias remains tilted to the hawkish side as growth proves resilient and inflation stays above target, but a couple more prints like today’s, combined with a slowing labor market, would quickly shift the narrative from how long to hold to how soon to cut. With moderating job gains and upcoming headwinds in the economy, we continue to expect the July rate hike marked the last one this tightening cycle. Rates are likely to stay elevated for a while before the Fed starts cutting towards the middle of 2024.

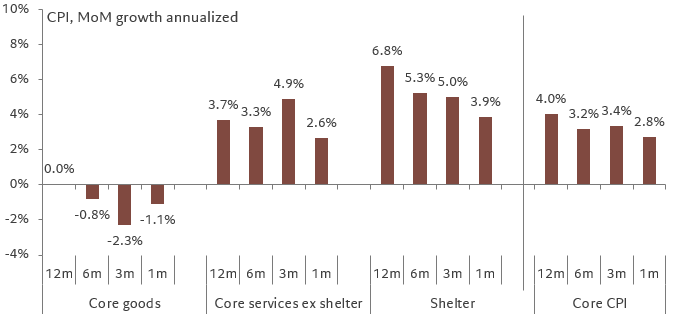

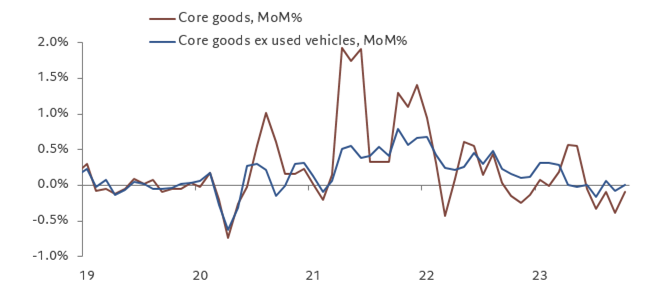

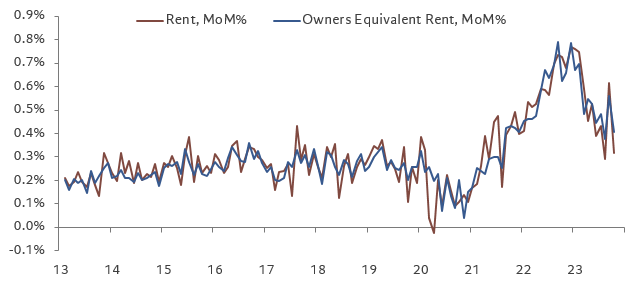

Looking at the details, current disinflation continues to be driven primarily by goods and housing, but supercore services inflation slowed as well. Core goods prices fell 0.1%MoM as used vehicle prices continued to decline (albeit at a slower rate). Shelter inflation decelerated sharply after an unexpected bump last month, with both rent and owners’ equivalent rent growth decelerating.

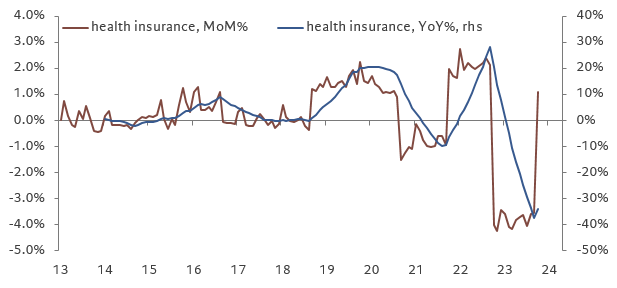

Supercore services inflation (core services ex housing), the Fed’s preferred gauge of underlying inflation pressures, slowed to 0.2% after rising to a one-year high last month. Price decline across travel categories (hotels, airfare, car rental, etc.) helped drive the deceleration. There was also a slowdown in other labor-intensive personal services. On the other hand, due to changes in measuring insurance prices health insurance swung from a drag to a small boost to CPI, and should remain positive for the next six months.

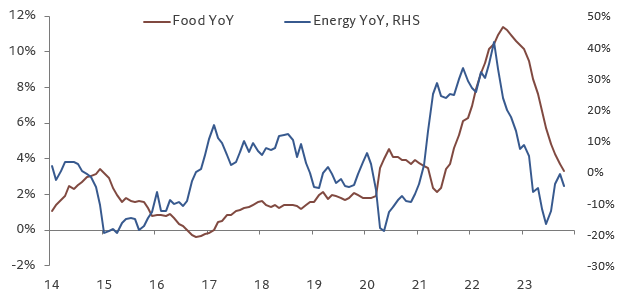

Headline inflation also came in weaker than expected, rising 0.045% MoM (consensus: 0.1%) and the YoY reading fell to 3.2% from 3.7%. Energy prices declined due to gasoline. Food inflation rose 0.3% and the YoY reading continues to fall.

Chart 1: Both headline and core CPI continued their downtrend

Chart 2: Core CPI inflation breakdown

Chart 3: Core CPI inflation breakdown, YoY%

Chart 4: Core goods prices stabilizing outside of used vehicles

Chart 5: Shelter inflation breakdown – further slowdown

Chart 6: Health insurance went from a drag to a boost, and is likely to stay positive in the next six months

Chart 7: Food and energy CPI inflation