Please find below a comment from Michael Hart, Senior FX Strategist at Pictet Wealth Management, on the Bank of Japan.

- At today’s meeting, the BoJ decided to leave rates unchanged at 0-0.1% (as expected) and to cut the size of its bond purchases. This was much hoped for as an alternative to a rate hike in an attempt to stabilize the exchange rate. However, the BoJ’s lack of decisiveness once again did it no favors, not unlike in April. While Governor Ueda intimated that the reduction in bond buying could be substantial once it gets underway, he did not provide any indication as to when such a reduction would take place or what the scale of it would be (it would be determined at the next meeting, he said)

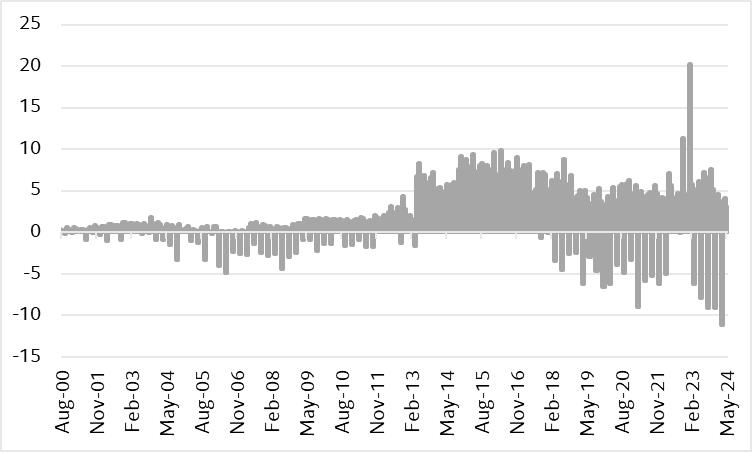

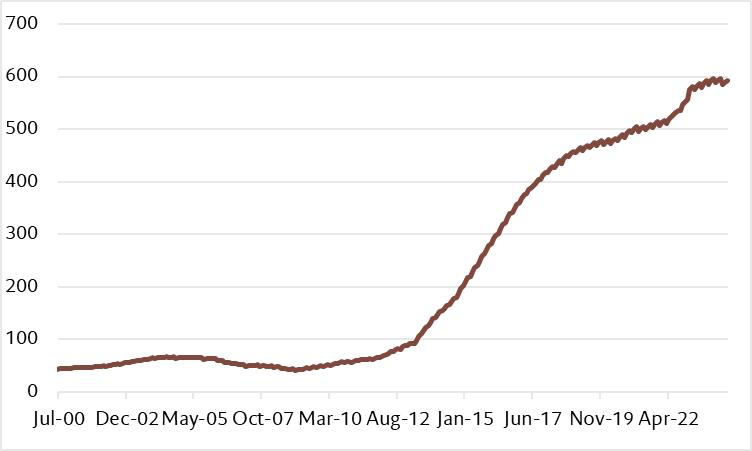

- What is “substantial” then? The BoJ sits on about JPY600 trn of bonds and purchases some JPY5.7 trn a month. Given the pace of roll-offs, reducing purchases by JPY100 bn (buying less than JPY6.6 trn) would bring the BoJ into QT territory. A more likely reduction in purchases by JPY200-500 could be more meaningful and bring monthly purchases closer to JPY 5trn. This is the figure to watch.

- Will it halt the yen slide? In the best case, such a step (if made explicit, which would somewhat constrain the BoJ in its flexibility) would reduce the balance sheet by JPY6 trn a year. This corresponds to roughly 1% per year, which pales in comparison to the Fed, who have reduced their balance sheet by over 10% over the past 12 months. This is thus a step in the right direction, but unlikely to be sizeable enough to make a meaningful change to the monetary stance. Given the large US-Japan rate differential and the structural acceleration in capital outflows from Japan, the yen is thus likely to stay under pressure. Indeed, since the intervention in April May which dragged USDJPY to 153, the pair has already climbed back to 158.

Stock of JGB holdings by BoJ, JPY trn

Monthly BoJ purchases of JGBs, JPY bn