Prof. Dr. Jan Viebig Global Co-CIO, ODDO BHF AM.

“Equities too often have a reputation among German and French investors for being speculative. However, we believe that when equity investments are approached in a planned, long-term manner—aligned with simple principles and within one’s risk tolerance—they become a potent tool for sustained wealth building”

Three British economists—Paul Marsh and Mike Staunton of the London Business School, and Elroy Dimson from Cambridge University—have embarked on a meticulous endeavour: they have traced 35 stock markets around the world as far back as possible to test a core theoretical question of investment. Are equities truly superior to all other asset classes over the long term? They analysed 23 stock markets starting from the year 1900, including today’s leading markets: the USA, the UK, Canada, Australia, Japan, New Zealand, and the stock exchanges in Northern and Western Europe. The findings of this study can serve as an example of applied economics, providing investors with an important guideline.

We draw four key conclusions from this study as well as from our own experience:

1) The statement that equities are an essential component of a long-term investment strategy is strongly supported by empirical evidence. The three economists have shown that, since the year 1900, U.S. stocks have risen by an arithmetic average of over 8% a year in real terms, after adjusting for inflation. Warren Buffett wisely stated, “My wealth has come from a combination of living in America, some lucky genes, and compound interest.”

While we have little control over our genetic makeup or longevity—matters better evaluated by others— when it comes to equities, one thing is certain: those who invest in stocks early and for the long term benefit longer from the compound interest effect, which Einstein is said to have once described as the “eighth wonder of the world”. Buffett himself started investing in the stock market in 1942 at age eleven. The second reason for investing in equities over the long term leads us to the topic of risk: the risk of loss from equity investments is significantly reduced if an investor commits his capital over a long period of time rather than speculates in the short term.

Although history does not always repeat itself, the following applies to the past: anyone who invested in the MSCI World index at the end of any month between 1970 and 2023 and held that investment for more than one year experienced a loss in only 26% of all possible one-year periods. Over a five-year investment period, the loss occurred in only 16% of all possible five-year periods. And over ten years, the probability of loss dropped to just 4%. In the period from 1970 to 2023, investors never lost money, not accounting for inflation, if they invested in the MSCI World at the end of any month and held on for 15 years.

Even though past performance is not a reliable indicator of future results, the data shows that the longer the investment horizon, the lower the risk of losing money with a broadly diversified equity portfolio. For these reasons—the compound interest effect and reduced risk of loss over time—we advise our investors to commit to equities for the long term.

2) In 1900, Germany represented 12.6% of the global equity market; today, it accounts for just 2.1%. This decline isn’t solely because of long-term challenges in Germany’s economic development—wars and misguided economic policies have indeed taken their toll—or because many new stock markets have emerged, which is also true. The primary reason for this shift is the extraordinary growth and importance of the U.S. stock market.

Warren Buffett has rightly stated that his investment success is not just due to the long-term nature of his strategy. He considers himself lucky to have grown up in the USA, a country that has had a particularly dynamic capital market for many years. In 1900, the U.S. made up 14.5% of the world’s equities; today, it accounts for 60.5%. The Swiss stock market, which was a distant second in 1900, now surpasses Germany with a 2.4% global share. A common mistake among investors, particularly in Germany and France, is an excessive focus on domestic markets. We recommend that investors pursue global diversification and not overlook the U.S. market. Indeed despite valuations that may seem high, American companies provide on average high return on equity.

3) It’s often argued that now is not the right time to invest in equities, with fatalistic statements such as “the market is at an all-time high” or “the risk of investing in shares now is far too great.” We believe this attitude is misguided.

According to calculations by US broker Charles Schwab, reaching a record high is not an exceptional event: between 1928 and 2021, the US S&P 500 index closed at a record high on an average of 14 trading days per year. Selection is more important than short- term timing aspects. We therefore invest in stocks that generate long-term value for their shareholders. This is always the case when the return on capital exceeds the cost of capital and revenues are growing.

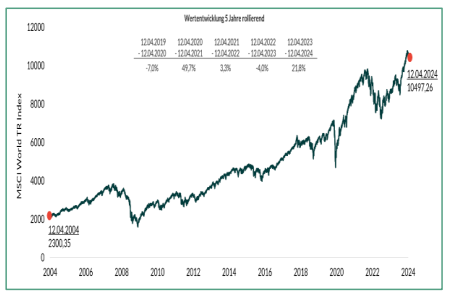

4) A few good days can be the difference between a mediocre portfolio and an outstanding one. An investor in the world equity index MSCI World Net Total Return including dividends from mid-April 2004 to mid-April 2024 was able to achieve an average annual increase in value of 7.9 percent if he was fully invested for the entire 20-year period (see chart). However, missing just the ten best trading days during this period would reduce the annual return to 6.8%. Missing the top 40 days out of these 5220 trading days would halve the annual return to just 3.5%.

The overarching message for investors is to commit for the long term and withstand market volatility to capitalise on the days with significant gains. This remains valid even during the inevitable weak market phases when it’s psychologically challenging to stay invested. Investors need to have the financial resilience to weather prolonged downturns without being forced to liquidate positions at inopportune times, which could crystallise any interim losses.

While German and French investors often face stereotypes of being speculative, we believe that when equity investments are approached in a planned, long- term manner—aligned with simple principles and within one’s risk tolerance—they become a potent tool for sustained wealth building. However, past performance is not a guaranteed predictor of future results. This caution is particularly pertinent today, as markets exhibit increased volatility amid escalating geopolitical tensions.