Paul Reuge, European Equities Portfolio Manager Rothschild & Co Asset Management.

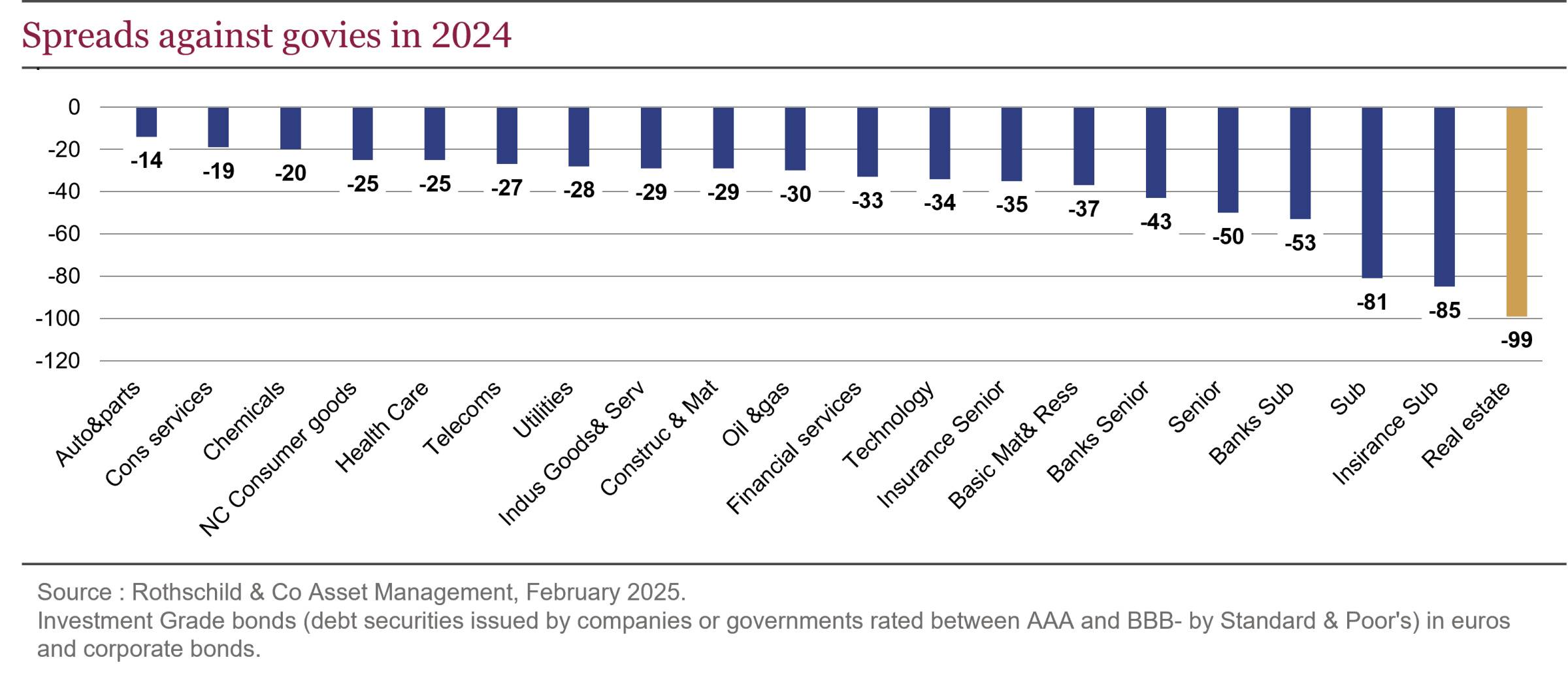

The sector’s correlation with interest rates was maintained in 2024, apart from during the summer break, when good publications from listed real estate companies helped to focus investors’ attention on fundamentals. The resurgence of uncertainty about the outlook for growth and inflation following the re-election of Donald Trump in the final quarter had a negative impact on the annual performance of property companies. On the fixed income markets, however, the picture was very different, with real estate benefiting from the biggest reductions in spread1 of any sector, reflecting investors’ enthusiasm for real estate debt.

Why such a divergence of appreciation on both sides?

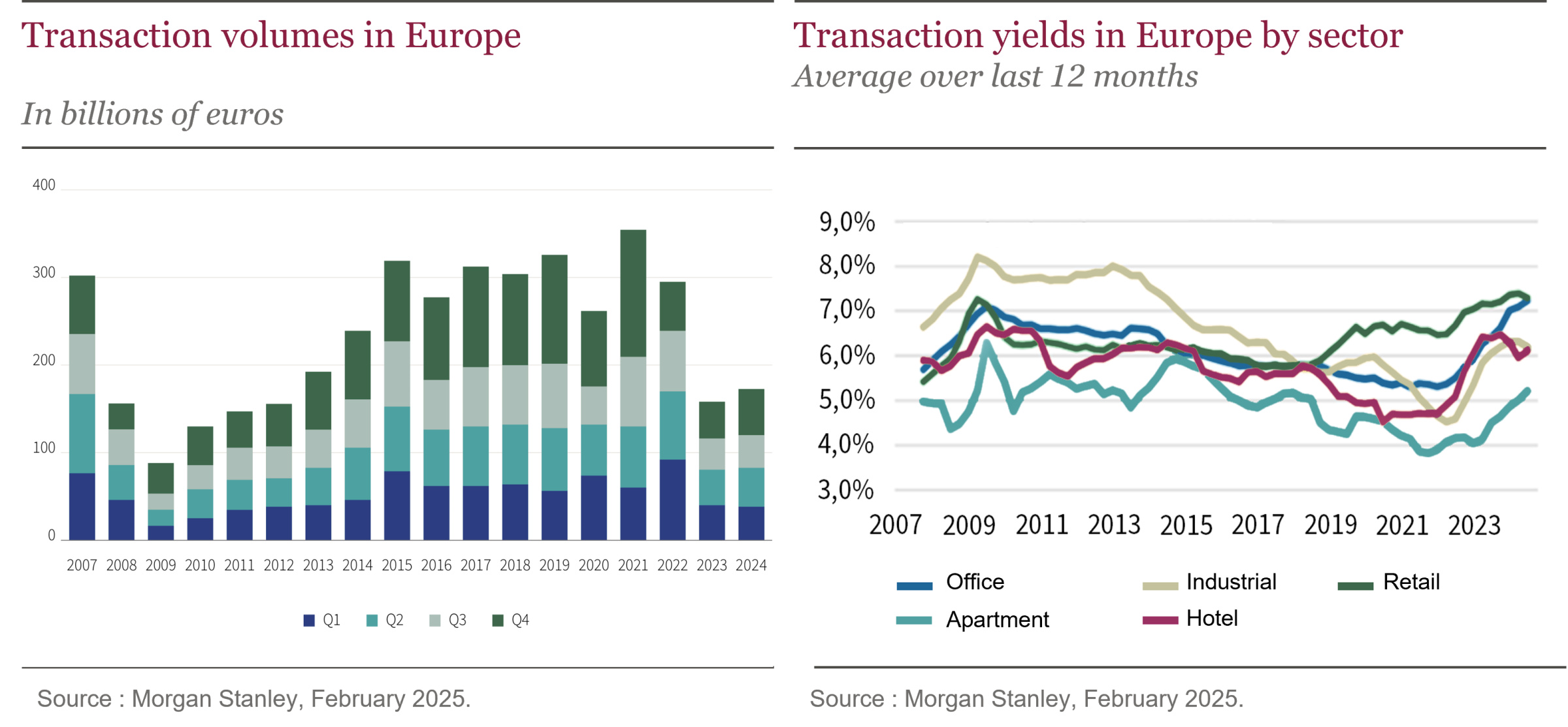

Debt holders have focused on improving property fundamentals, with most markets having bottomed out in 2024. Transaction volumes are still recovering, but the rebuilding of the risk premium and strong demand for the best assets have begun to bring buyers back:

Listed real estate companies have continued or even completed their debt reduction programmes, and some are already repositioning themselves for a new growth cycle. The liquidity/financing risk has therefore been considerably reduced, and with it bond yields. On the equity markets, risk assessment continued to be guided by the trend in long-term yields, despite the brightening after the half-yearly results.

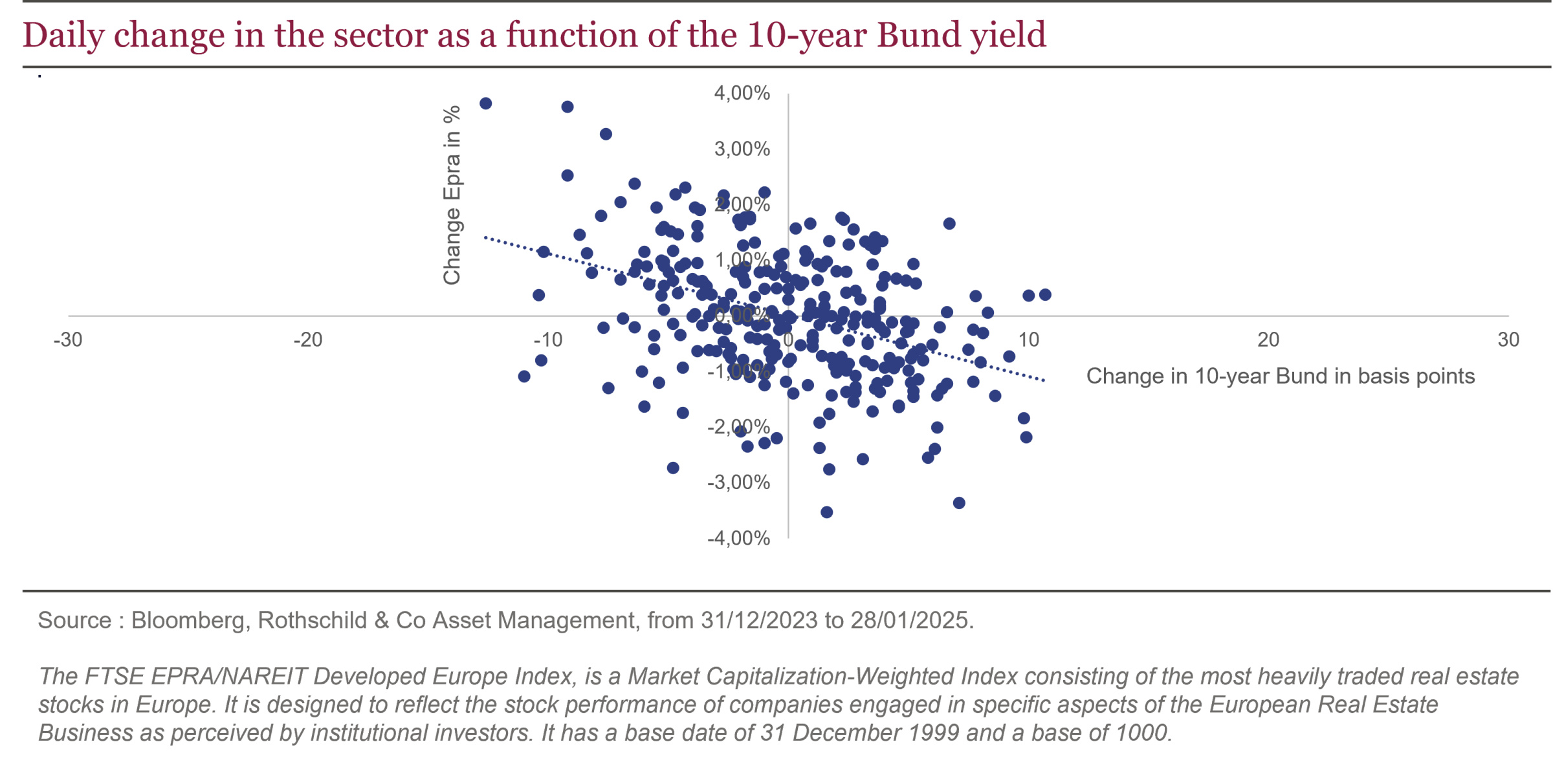

The sector’s high correlation with 10-year yields since 2021 (the start of monetary policy tightening) translated into a valuation sensitivity of around +/- 1.1% for a movement of 10 basis points2 in 2024, i.e. a fall in valuations of around 3.3% for a rise in the bund of 30 basis points2 , more or less summing up the year 2024 (rise in the bund of 30 bp and fall in the eurozone IEIF of 3.9% excluding dividends)2.

Medium-term outlook

It will of course remain dependent on the direction of interest rates. A moderate rise (<30bp) would have little impact on the direct listed real estate market, but would curb the reappraisal of property companies until an inflection point is reached. A significant rise (of 50 to 100 bp) without any inflationary counterpart would cause a ‘double dip ’3 in property valuations. The good news, apart from the fact that this scenario remains unlikely given the deteriorating economic situation in Europe and inflation returning close to the European Central Bank’s target, is that the current level of discount already anticipates this scenario.

Indeed, a 30% discount on net assets corresponds to a 15% discount on gross assets, the equivalent of an implicit average yield of 5.5% (i.e. 70 basis points higher than the appraised yield)4.

The fall in refinancing costs seen on the bond markets will also enable property companies to return to earnings growth more quickly than expected, as the rise in interest costs will no longer absorb all the growth in rental income. This factor, combined with the sector’s already high dividend yield (5.2%)2 , is an additional incentive.

Which real estate markets to choose?

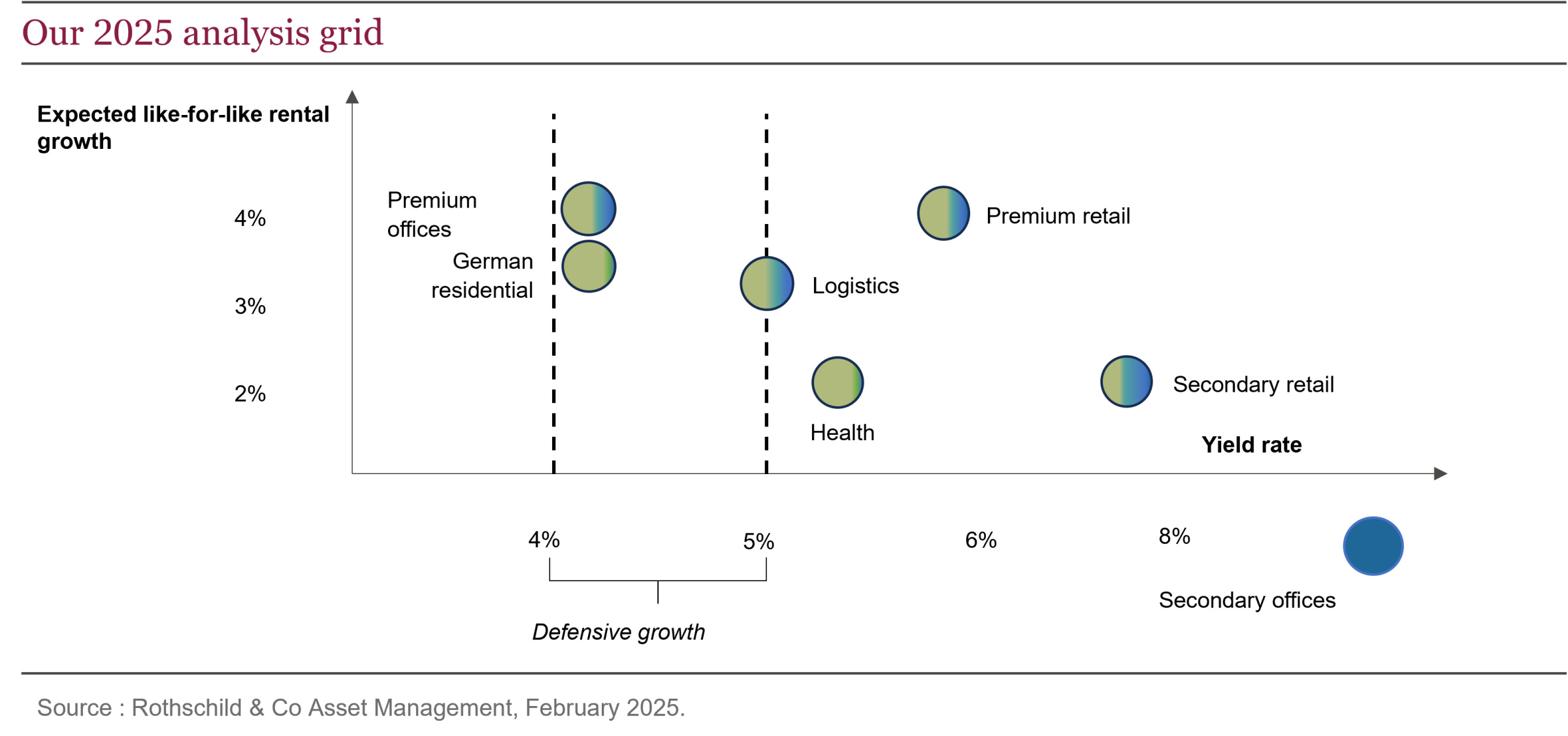

Sectors with a ‘defensive rental growth’ profile, i.e. less sensitive to the economic environment and whose lower yields would benefit from a stabilisation or fall in interest rates (which remains our preferred scenario) should attract investors. These include prime residential5 and office property in central areas where rental supply is very limited. This pocket of investment represents half of R-co Thematic Real Estate’s assets4.

In 2024, after benefiting from the recovery in consumption and footfall post-covid, shopping centres returned to the hierarchy that existed before the pandemic, with the largest assets outperforming the smallest. Against a backdrop of sluggish consumption, the best assets outperformed inflation by a wide margin, in contrast to the smallest assets. This trend is set to continue in 2025, with consumption remaining largely dependent on economic growth, but supported by the very high savings rate in the eurozone (15.7%)6 and rising real incomes. The correction in shopping centre yields (the biggest since 2018) is now enabling listed real estate companies to offer very high dividend yield (around 8%)2 at still modest valuations. The sector therefore remains attractive, with one-third of the portfolio allocated to it.

Logistics remained popular with investors on the direct listed real estate markets, despite a marked slowdown in rental demand in 2024. This led to a sharp correction on the stock market, with the sector now offering an attractive entry point in the expectation that demand will stabilise. We took advantage of this to increase our allocation, which remains limited to less than 10% of the portfolio4.

Finally, the healthcare sector seems to us, in relative terms, to offer the fewest opportunities. Its defensive profile is attractive, but it offers less organic growth than residential property. External growth, which used to be the sector’s driving force, is still limited by the discounted value of listed real estate companies. Lastly, the yield on assets of just over 5% is less sensitive than residential property to the current monetary easing, and much lower than retail property.

Conclusion

Macroeconomic uncertainty wiped out the sector’s initial re-rating at the end of 2024. Although this uncertainty is still strong with the presidency of Donald Trump, the fact remains that the sector can now rely on solid pillars to once again attract investors on a more sustainable basis:

- The low point reached in listed real estate market valuations,

- A drastic fall in refinancing costs, allowing a return to growth in earnings per share.

In the meantime, the sector’s high yield (>5%)7 offers a significant carry, especially as distribution is now set to increase. R-co Thematic Real Estate’s current positioning on stocks offering a ‘defensive growth’ profile should enable us to take full advantage of the sector’s re-rating.

[1] Spread: A spread measures the difference, expressed in basis points, between two rates or yields.

[2] Source: Bloomberg, February 2025.

[3] Double dipping: the practice of receiving two incomes from the same source.

[4] Source: Rothschild & Co Asset Management, February 2025.

[5] Prime offices: buildings that meet the latest standards and benefit from a central location.

[6] Eurostat, Q2 2024.

[7] Dividend yield