Please find below Xiao Cui’s, Senior Economist at Pictet Wealth Management from the FOMC meeting.

The FOMC left rates unchanged and is in no hurry to cut. Interest rate projections moved up to show just one rate cut in 2024 (down from 3), fewer than our expectation of two. But the cut was simply pushed out to 2025 as the median now sees 4 rate cuts in 2025, up from 3. Chair Powell did not take the possibility of a September rate cut off the table, but he refused to say specifically how many months of good inflation data is needed to build confidence to cut rates. We maintain our call for two rate cuts this year in September and December.

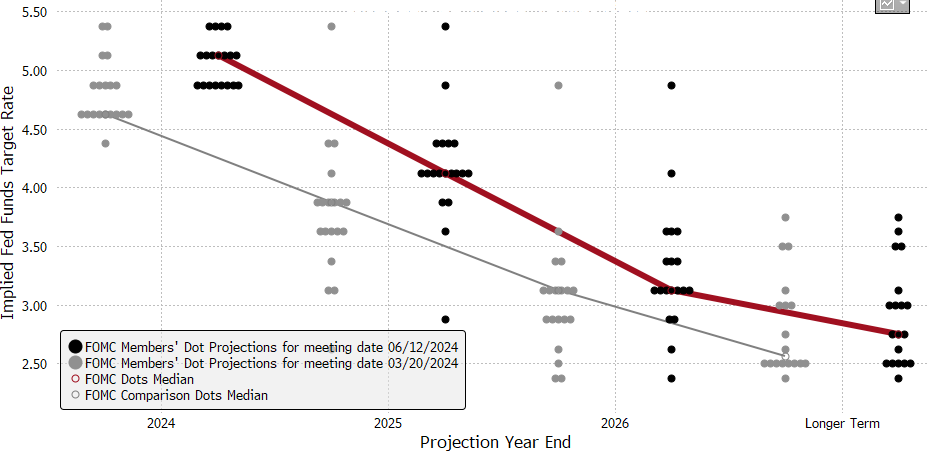

After the low CPI reading earlier in the day, it was a surprise to see the median dot for 2024 move up to show one, instead of two cuts (our expectation). To be sure, the committee is very much divided. The mode was two rate cuts penciled in by 8 officials. 7 officials wrote in one rate cut, and 4 officials see no rate cut at all this year. The only sure conclusions we can draw from the rate projections is that the max number of cuts this year is two. The earliest move is September. And no one has a rate hike in their base case.

When asked about the split in the committee’s rate projections, Chair Powell noted he couldn’t really distinguish between the two projections (one or two rate cuts) and all of them are plausible outcomes.

We think the dots are already old news and data will trump the dots.

- Although officials were able to update their projections after the CPI report, it’s unclear to what extent that was reflected. Powell noted that some people do (update forecast after an important number), some people don’t. And most people don’t.

- The Fed lacks guidance as it has abandoned forecast-based policy making and became extremely data dependent. The inflation and employment data will drive interest rate decisions and trump the rate projections that officials put down today.

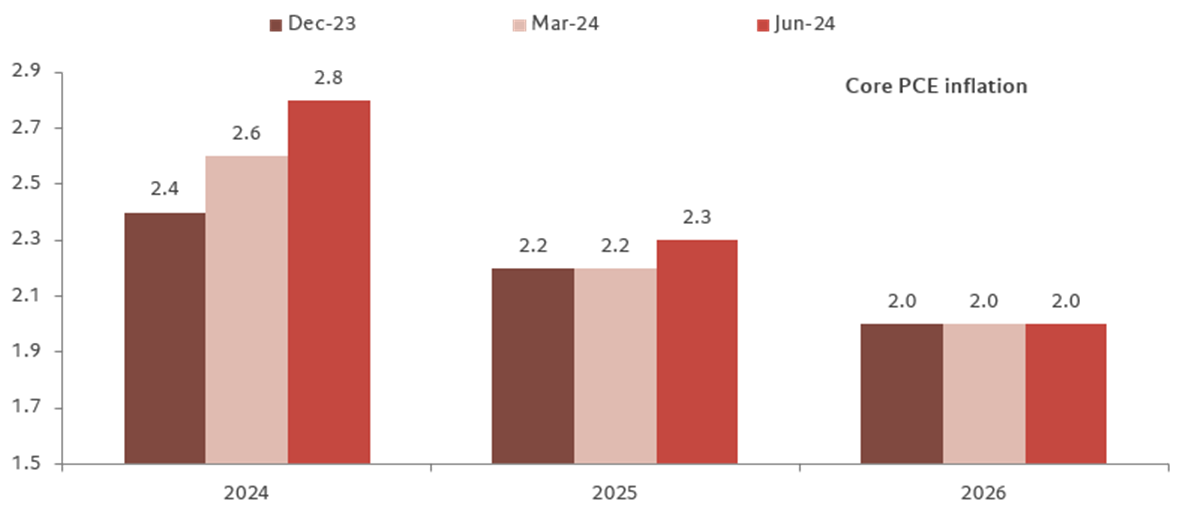

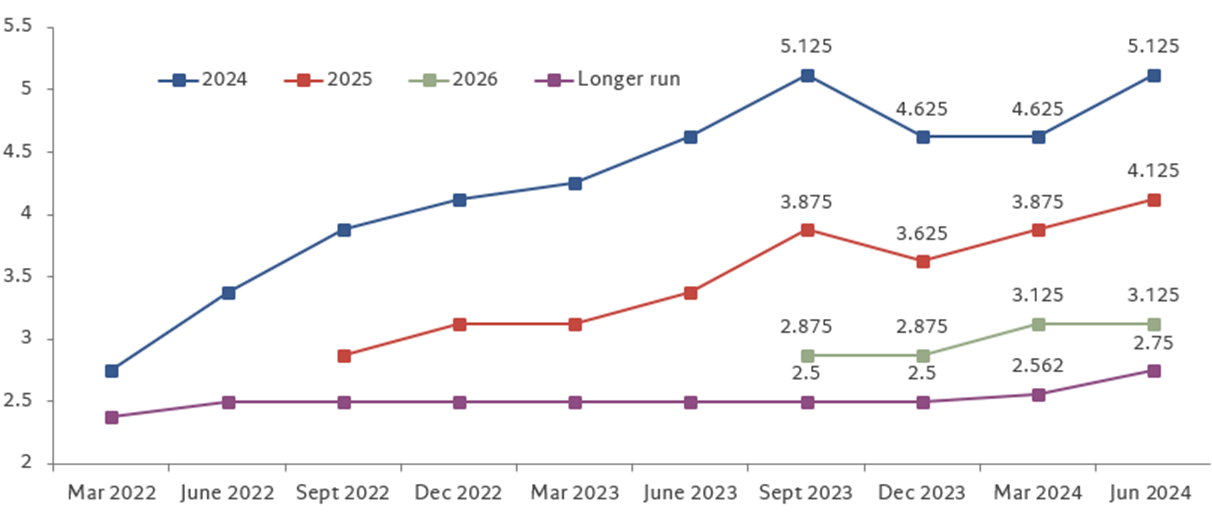

The upward drift in interest rate projections is due to upward revisions to inflation projections. The committee now sees core PCE ending the year at 2.8% Q4/Q4, up from 2.6%. The 2025 forecast only moved up slightly to 2.3% from 2.2%, and the 2026 forecast stayed at 2.0%. Interestingly, the 2026 median rate projection stayed unchanged at 3.125%. The longer-run dot moved up to 2.75% from 2.56%, consistent with some officials’ view that the neutral rate has shifted up.

The Fed is trying to balance the risk of cutting too soon and too late delicately. For now, the labor market is gradually balancing so the burden of proof lies on the inflation side. But the Fed is acutely aware of the two-sided risks to the economy now that policy has been restrictive for a while. It is also trying to stay ahead of the curve and not wait for things to break before cutting rates, hence the asymmetry in the reaction function to labor market weakness.

There will be three more inflation report before the Sept 18th FOMC meeting. We expect continued good readings on inflation to enable the Fed to start cutting then, but the risk continues to be that the disinflation path is bumpy and a cautious Fed might need to see more months of good readings to only start cutting in December.

FOMC dot plot Jun 2024 vs. Mar 2024

FOMC median dot evolution

FOMC core PCE median projections