Reserve a spot for Japanese stocks in your savings plan

The Japanese stock market has been due for rediscovery for a while now, after being forgotten by just about every investor for years. The Nikkei index even improved set a new record for the first time in 35 years! And despite the recent recovery, the Japanese stock market is still fairly cheaply priced. The larger capitalisations in particular are ideally placed, thanks in part to the weakness of the Japanese yen, to further deepen their recovery. And that is certainly the case if the Chinese economy, which is in their backyard, were to recover. Integrating a limited position in Japanese equities via an ETF into a savings plan is worthwhile given the (geographical) diversification and potential.

Heightened interest

There are a lot of reasons to stop ignoring the Japanese stock market. And perhaps the most important underlying reason is that Japan is attracting money again; interest from both Japanese investors themselves and foreigners is at its highest level in more than a decade. Earlier this year, the Nikkei 225 index even demolished the 40,000-point mark (see below), bettering a record that had been in the charts since 1989. And many will point out that this has already happened a few times over the past few decades that the Japanese market was ‘rediscovered’. Why shouldn’t this time again be a false start? And as an investor, why risk another lost decade where your investments for several years yield nothing?

And to answer this question, many arguments, both macro and corporate, can be put forward. First, Japan has finally been able to put years of deflation behind it and interest rates have risen: 10-year government bond yields have risen above 1% for the first time since 2011. The market is betting that the central bank, concerned about the yen’s weakness, will further normalise its monetary policy to narrow the hefty interest rate differential between Japanese government bonds and those of other countries. In fact, in March 2024, it already ended negative interest rates and raised its interest rate for the first time since 2007: the leading rate is now 0%

Normalisation

So these first steps towards ‘normal’ market conditions have clearly boosted confidence at home and abroad. And it looks like interest rates will rise further. First of all, because wages have increased sharply. And this will boost household consumption (50% of GDP), boost the economy and provide lasting support to inflation. But also because new investors will have to be attracted to Japanese government paper (government debt is 260% of GDP) now that the Japanese state will buy much less itself and these investors will want more than 1% at 10 years. Bond yields will therefore have to rise gradually and this will certainly support the severely undervalued yen.

Japanese GDP growth is currently lagging somewhat. After falling 0.8% in Q3 2023, Japan’s economy unexpectedly fell by another 0.1% in Q4. This was due to a decline in household consumption, investment and government spending. But as indicated earlier, the main union recently managed to secure a solid 5% wage increase for 2024, so it looks like households will have more room to manoeuvre. Business leaders are struggling with labour shortages and are starting to be more generous to their employees. Although growth projections of 1 to 1.5% for 2024, one of the highest rates for an industrialised country, it now remains to be seen whether these expectations will materialise. In the 1st quarter, the economy already fell 0.5% compared to the 4th quarter of 2023.

Reforms + China

But not insignificant in the recovery story are the structural changes and sustainable reforms at corporate level that have recently been implemented in the Land of the Rising Sun. And these are profoundly transforming financial markets and booming investments. Corporate governance has taken hold while small shareholder rights are now more respected. More and more independent directors are being appointed and corporate interventions are being approved to bring out the hidden value of companies. It should come as no surprise that Japanese companies are paying record dividends and riding high on their share buybacks.

In addition, more and more investors are realising that Japanese stocks are a good and much safer way to play a possible China recovery. There is a lot of doubt around the country today but if the Chinese recovery comes through then the first country to benefit will be Japan, as it is China’s biggest trading partner: accounting for 20% of Japanese trade. On top of that, Chinese tourists are finally coming back to Japan, now that organised tours are allowed again. And these Chinese tourists account for a third of all international tourist spending in Japan. So it is a real gold mine.

What to invest in ?

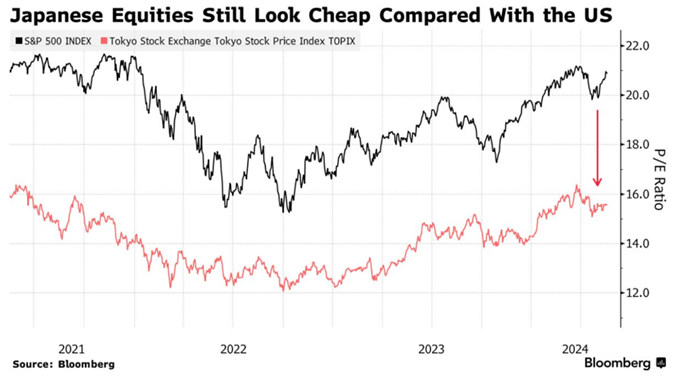

Japan’s rerating has only just begun and the recent pause in the stock market, since its late-March peak, by no means implies that the recovery is over. The Japanese stock market is also not at all expensive at 15.5 times expected earnings, and against the US market (S&P500) it is even significantly undervalued (see chart below). On top of that, average earnings growth of between 10% and 15% is expected this year. Furthermore, almost half of Japanese companies are still quoted below their book value. Japanese stocks may certainly have a place in a savings plan or a large portfolio. They offer excellent geographical portfolio diversification because the Japanese stock market often does not care what global or western stock markets behave. However, preference is given to the larger conglomerates that benefit more from the weak yen and realise record profits.

At Trade Republic, there are 107 ETFs grafted on Japanese assets, bonds and equities, which are eligible to be included in a savings plan. The vast majority do track an equity index. So it is not an easy choice to pick a Japanese ETF given the wide range on offer. We would go for a tracker that tracks the index, consisting of Japan’s largest companies, such as MSCI Japan and given the weak yen in recent years, an ETF that does not hedge currency risk and is denominated in EUR. Choose from the following three, which have different characteristics such as different currencies, distribution or capitalisation and different underlying indices. Japan Equity JPY (ISIN code: IE00BYQCZN58) and MSCI Japan USD (Distribution, IE00B5VX7566) track MSCI Japan. Core MSCI Japan IMI USD (Acc) (IE00B4L5YX21) is modelled on a much broader index consisting of 1068 stocks. You are effectively buying the entire Japanese market with this.