By Prof. Dr. Jan Viebig, Chief Investment Officer, ODDO BHF Asset Management.

The German economy is in a position of weakness, just as the global economy appears to be entering a more conflictual era. Trump has barrelled ahead with his promised tariff increases, which threatens to trigger trade disputes between the US and China, Europe, Canada, and Mexico. At present it is impossible to predict what will happen to global trade if a spiral of punitive tariffs and retaliatory measures is set into motion. At the beginning of the week, President Trump announced punitive tariffs of 25% on imports of steel and aluminium (‘no exceptions or exemptions’, he vowed); the corresponding rule will come into force on 12 March. European investors reacted immediately to the announcement by dumping shares of European steel manufacturers, namely Arcelor Mittal, Salzgitter, and Thyssen-Krupp. The sell-off on Monday shows how nervous investors are feeling. Meanwhile, Trump further stated that he could also impose higher tariffs on cars, computer chips, and pharmaceuticals.

Donald Trump’s return to the White House is an additional element of uncertainty for Germany. The country is especially dependent on exports, and as such relies on open markets and moderate tariffs. If Trump implements his proposed tariff policy, world trade could decline by 2.5% in 2025 and by as much as 4% in the long term, according to the Kiel Institute for the World Economy (IfW). The American tariff hike would drive down the world’s gross domestic product (GDP) by 0.75% in the short term and around 0.6% in the long term. Higher tariffs would hit European economies much harder than the US economy.

Tariffs aside, the German economy is facing plenty of other negative news. Production in the manufacturing sector shrank by 4.5% in 2024. In industry alone, the decline was 4.9%. This marks the continuation of a decline that began in the spring of 2023. Two key sectors are particularly affected: automobile manufacturing, which fell by 7.2%, and engineering, which declined by 8.1%. German exports are also in the doldrums, declining by 1% in 2024 to just under EUR 1,600 billion. In December 2024 alone, exports to the US fell by 3.5%. But the US is not the only export market affected; the Bundesbank also attributes the decline in German exports to ‘the reduced competitiveness of German industry’ and competitive pressure, especially from China.1

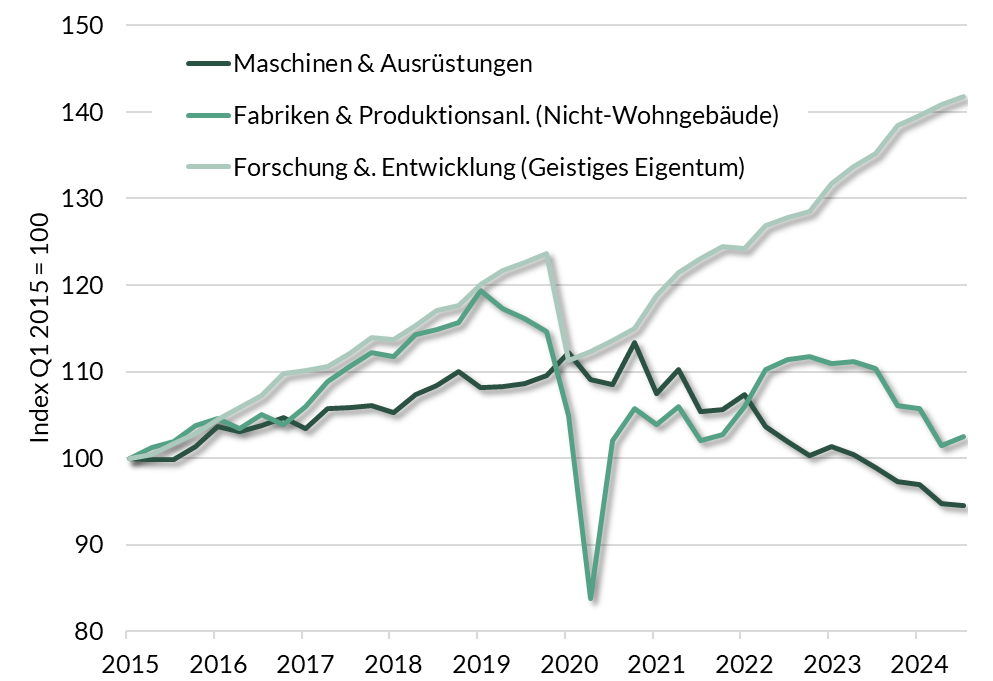

After two years of negative growth in 2023 and 2024, the German economy is facing yet another year of recession. This situation brings into stark relief Germany’s weaknesses as a business location, which have been piling up over the years. While companies continue to invest in research and development, investment in factories and production facilities in Germany has fallen sharply. Additionally, investment in machinery and equipment is now around 17% below its 2020 peak in price-adjusted terms (see Fig. 1).

Fig. 1: Investment in the non-governmental sectors (Q1 2015–Q3 2024)

Source: Destatis / LSEG Datastream

Nevertheless, we will not be joining the chorus currently singing the swan song of German industry. We believe that the reforms Germany desperately needs have been delayed for too long. During the current election campaign, the various parties have said very little about what they would do to improve conditions for manufacturing in Germany. Lowering corporate taxes should be a priority. The economy is also suffering due to excessively high energy prices compared to other countries. The cost of energy is a key reason that companies are not investing in new production facilities in Germany. Additionally, the country needs an economic policy that creates a supportive environment for production and economic growth. We don’t need more political sniping across party lines but, rather, new ideas, such as creative approaches to address population aging and the shortage of skilled workers. At a time of growing geopolitical uncertainty, the German economy needs a policy programme that fosters confidence.

However, there are still many successful, well-run companies on the German stock market – and elsewhere in Europe – that offer attractive investment opportunities for long-term investors, according to their individual appetite for risk. Many German companies have a strong international focus, generating a large share of their sales outside of Germany and investing significantly in production facilities overseas. They often manufacture highly specialised products that continue to find willing buyers despite higher tariffs. Whether the interdependence of German companies poses a risk in the context of the tough trade disputes ahead of us is currently the subject of fierce debate amongst market participants.

We believe that international diversification still provides the most effective protection against the global economy’s many imponderables. Earnings momentum in US equities is still high, as the current reporting season shows. Companies in the S&P 500 increased their earnings by 16.4% in the fourth quarter of 2024 according to Factset based on reported figures and estimated profits of companies that have not yet reported. That would mark the strongest quarterly earnings growth since the fourth quarter of 2021. For this reason alone, German investors should continue to diversify their equity investments internationally rather than focus narrowly on a single country or region.

1 Deutsche Bundesbank: Monatsbericht Januar 2025, p. 4.