Steve Huguenin-Virchaux, Head of Total Return Equities CPM and Business Strategy Pictet Asset Management.

In an era of volatile markets and lower yields, hedge funds offer diversification, with the potential of improved returns and downside protection.

Hedge funds are firmly back on investors’ radar– and for three main reasons.

Firstly, investors’ need for yield can no longer be fully met by low-risk money market funds. Interest rates have peaked and are now on a downward trajectory, especially in the euro zone and Switzerland (see Fig. 1). This will eventually push yields to levels that are too low for many income-hunting investors. For example, the real yield on the 10-year Swiss bond is already in negative territory. Hedge funds can step in to replace that yield thanks to their access to a wide variety of asset classes and instruments, the capacity to use leverage and to combine long and short positions, and the ability to contain volatility.

Secondly, after two years of approximately 20% returns from stock markets, there are signs the rally may be fading in certain regions, giving way to a correction that has already started in the US. Investors are now looking for beta replacement in an effort to protect gains. Hedge funds offer a way to exchange outright market exposure for products that can offer both downside protection and alpha-driven returns.

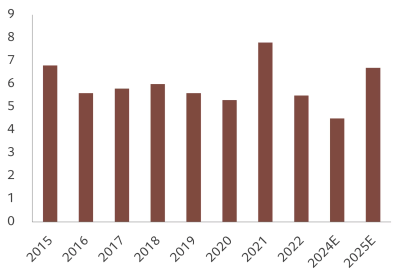

Fig. 1 – Rates retreat

Interest rates in major economies, actual and forecast, %

Source: Pictet Asset Management. Data covering period 01.01.2020-21.03.2025.

The stock market has become more volatile, and returns are more dispersed with shares of different companies no longer moving in lockstep with each other. The correlation between single stocks within the US market is at the lowest level in a generation, while the dispersion of returns is at generational highs. This picture is similar in Europe. Such an environment creates a very favourable opportunity set for long/short hedge fund strategies. Greater dispersion of returns increases the number of relative value opportunities that investors can capitalise on. Indeed, over the past 25 years, hedge funds have delivered the highest alpha – excess return over the risk free rate – during periods of high dispersion and low correlation between stocks.Barclays Strategic Consulting, 01.2025

Thirdly, there has been a marked pick-up in deal making and corporate activity, including mergers and acquisitions, initial public offerings, spin-offs of subsidiaries and secondary share listings.

This reflects prospects of deregulation (from a pro-business US administration, but also in Europe), cash-rich corporate balance sheets and the pressure on private equity sponsors to deploy capital. Global announced M&A deals are estimated to have risen by 25% in 2024 to USD4.5 trillion, and are forecast to reach as high as USD6.7 trillion this year (see Fig. 2).Morgan Stanley, Dealogic, 11.11.2024 Such deals are the bread and butter of event driven strategies, which can pick the winners and the losers from any transaction.

Fig. 2 – M&A momentum

Global M&A deal count, USD tn

Source: Morgan Stanley Research, Dealogic. Data covering period 01.01.2015-11.11.2024.

Meeting investors’ needs

From an investor point of view, falling interest rates, heightened market volatility and unstable correlations between asset classes make traditional long allocations to bonds or equities less attractive. That’s where hedge funds can step in, using a range of investment and risk management techniques to control volatility and deliver returns that are independent of the market cycle.

The diversification benefits can be accessed in two main ways, depending on which type of hedge fund investors choose.

Some serve as diversifiers because their returns show little or no correlation with those of equities and bonds. In this category we find multi-strategy and equity market neutral strategies. Our analysis shows that, over the past five years, investors would have achieved better risk adjusted returns and an improved Sharpe ratio by replacing part of their traditional 60% equity, 40% bond portfolio with an allocation to Pictet’s Alphanatics strategy.USD net returns, data covering period 31.12.2019-31.12.2024.

Other strategies can serve as substitutes, capable of replacing a portion of equity investments in a portfolio and improving the risk return profile – something that could appeal to investors concerned about stretched valuations, or those looking for a less volatile alternative to direct stocks exposure.

Directional long/short equity funds fall in this category as they aim to offer returns similar to those of equity markets but with less volatility and limited drawdowns. One example is Pictet’s Atlas Titan, which provides upside participation while having a history of delivering capital preservation in stressed markets. A flexible approach and a wide remit mean the managers can take advantage of swings in market pricing and in sentiment. Similarly, Pictet’s Mandarin, a long/short strategy primarily focused on China, Hong Kong and Taiwan, is providing an alternative for investors who are looking to take advantage of renewed opportunities in China driven by innovation, but are conscious of geopolitical risks.

Conservative equity market neutral funds or multi-strategy funds can also be used to improve the risk/return profile of a bond allocation.

Investors are increasingly taking note: according to a recent Goldman Sachs survey, hedge funds are the most sought-after strategy among asset allocators, surpassing long-only strategies and private assets.

With interest rates heading lower, elevated geopolitical tensions, uncertainty around trade tariffs, policy disruption and stretched valuations, the world is likely to see a prolonged period of heightened volatility and unstable correlations between major asset classes. Investors will therefore need to diversify their portfolios and introduce investments that offer an element of capital preservation – while still retaining the option of benefiting from any positive surprises.

Hedge funds are well placed to fulfil that need, capitalising on the many long and short opportunities around the globe and acting as a valuable diversifier to a stocks and bonds portfolio, with the potential to improve risk adjusted returns over the economic cycle.

Total return at Pictet Asset Management

Scale and experience

- With over 20 years of experience in hedge fund management, PAM currently oversees nearly USD7 billion across six diverse strategy families: Multi-Strategy, Market Neutral Equity, Long/Short, Event-Driven, Fixed Income, and Systematic. Our team of over 50+ professionals manages UCITS non-UCITS funds.

Independent and highly focused

- We view our Total Return franchise as a collection of independent and highly focused teams of experts who can draw on Pictet’s global infrastructure.

Stringent on risks

- A strong capital preservation culture, including prudent use of leverage and a focus on avoiding any liquidity mismatches.

Barclays Strategic Consulting, 01.2025

Morgan Stanley, Dealogic, 11.11.2024

USD net returns, data covering period 31.12.2019-31.12.2024.