Please find below a new comment from Xiao Cui, Senior Economist, at Pictet Wealth Management, ahead of next Wednesday’s Fed meeting :

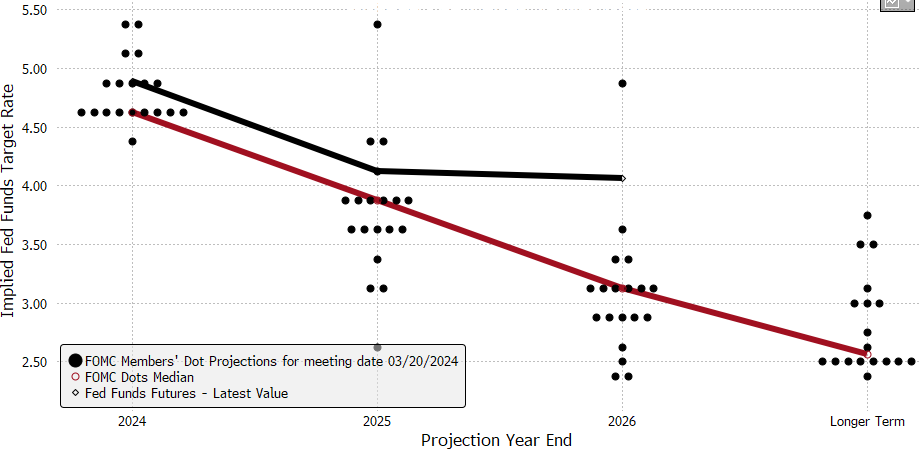

The new dot plot and Chair Powell’s press conference will take center stage at the FOMC meeting next week, where we expect no change to the policy rate or QT tapering plans. We expect the median dots to shift up, indicating two rate cuts this year, down from three cuts in the last projection in March. The risk is tilted towards a larger shift up to indicate just one rate cut this year, which we would interpret as a move in December. We expect the 2025 and 2026 median dots to shift up by 25bps each to reflect the shift up in 2024 rates. The longer run dot should shift up slightly as well. Our forecasts for the median dots can be found in chart 1. We expect the policy statement to remain largely unchanged with the soft easing bias still intact in the forward guidance.

We expect the outcome of the meeting to be consistent with an FOMC that could get comfortable cutting in September. The nonfarm payrolls report this Friday and the CPI report next Wednesday before the FOMC announcement could potentially swing the risks.

Since the last FOMC meeting, macro data have pointed to tentative signs of resumed progress towards disinflation, a healthy slowdown in the labor market, and a deceleration in growth from strong rates earlier. The Atlanta Fed GDPNow tracking for Q1 has dropped sharply from 4.2% in mid-May to 1.8% currently. This should support the argument that monetary policy is sufficiently restrictive and further rate hikes are not necessary.

Therefore, we expect Chair Powell to note that policy is likely sufficiently restrictive, and it is appropriate to give restrictive policy further time to work by keeping rates high for longer. He could echo Governor Waller’s comments that it would likely take several months of softening inflation data to get the Fed to initiate rate cuts. The chair is likely to embrace a view of continued disinflation on a sequential basis (with lower confidence than before), but note that patience is warranted. The Fed could shift their policy stance quickly if the labor market unexpectedly deteriorates, which should be an increasingly bigger risk factor in the Fed’s risk management approach.

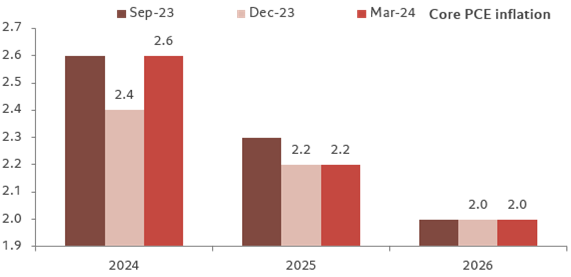

The updated economic projections should see higher core PCE inflation, with the 2024 median ending up at 2.8%, up from 2.6% and a second consecutive upward revision. GDP and unemployment rate projections can remain largely unchanged.

We expect two rate cuts this year in September and December, as inflation decelerates and the labor market engineers a healthy slowdown. The Fed is likely to become more cognizant of both the risk of an inflation reacceleration, and that of an unexpected labor market slowdown. We expect the hawks and doves on the committee to continue debating the balance of risks.

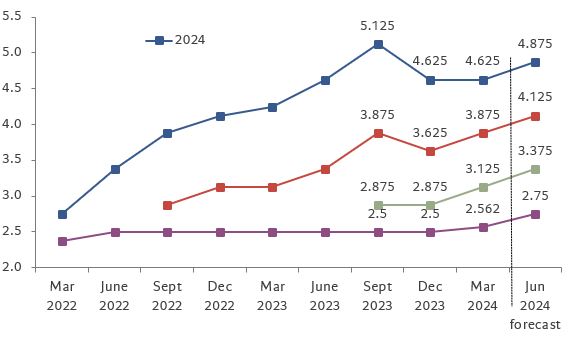

FOMC median dot plot with forecast

FOMC March dot plot, median, and market pricing

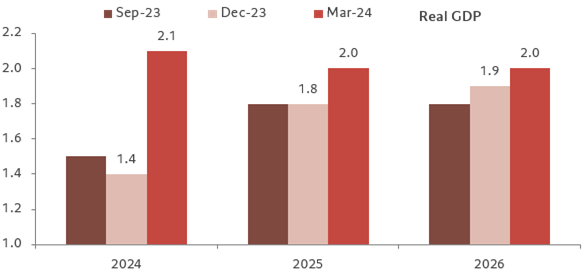

FOMC GDP projections, median

FOMC GDP projections, median