Below you will find a new commentary by Lauréline Renaud-Chatelain, CIO Office & Macro Research at Pictet Wealth Management.

SUMMARY

- Corporate bonds have outperformed government bonds this year, mainly due to spread tightening and corporate bonds’ more elevated yields. Credit spreads now look particularly tight compared to their historical ranges, especially for US investment-grade (IG) corporate bonds. And corporate bonds’ historically attractive yields are mostly due to the significant rise in central banks’ policy rates.

- Given that euro IG spreads remain close to their historical median, euro IG should continue to outperform cash this year as we expect the European Central Bank (ECB) to cut short-term rates by 100 bps by year’s end. By contrast, the prospect of delayed US Federal Reserve (Fed) rate cuts means that cash in US dollars will likely continue to offer juicy returns while we expect US IG spreads to widen given their high valuations.

- We remain overweight euro IG credits but have moved from overweight to neutral on US IG and from neutral to overweight on cash.

ROBUST DEMAND FOR CREDIT

Corporate bonds have outperformed government bonds this year, mainly due to spread tightening and corporate bonds’ more attractive yields. Whereas year-to-date 10-year US and German government bonds had posted negative total returns of – 3.1% and -4.5%, respectively by end May, US and euro IG corporate bonds perfor- mance was only mildly negative at -0.6% and -0.2%, respectively (according to ICE indices). In other words, investors have been gaining excess returns from credit over government bonds of similar duration.

The reasons behind the relentless tightening of credit spreads in the last few months are manifold. First, US and European economic growth has been more resil- ient than expected, as fears of a sharp economic slowdown in the wake of central banks’ aggressive rate-hiking campaigns have faded. For example, earnings growth for US IG companies has accelerated in Q1 this year and has stayed in positive terri- tory since late 2020. However, as indebtedness has risen even faster, the median net leverage ratio (net debt over 12-month profits) for US IG companies outside the fi- nancial and utilities sectors continues to increase, standing at 2.1x in Q1, well above the pre-pandemic average. And although the median interest coverage ratio (inter- est expenses over 12-month profits) has declined to a median of 9.8x as companies have had to refinance at higher rates, it is likely to remain manageable for most non-financial US IG companies as long as positive nominal GDP growth ensures in- creases in profits. In 2024, we expect nominal GDP growth to be a solid 5.8% in the US, but lower (3.2%) in the euro area.

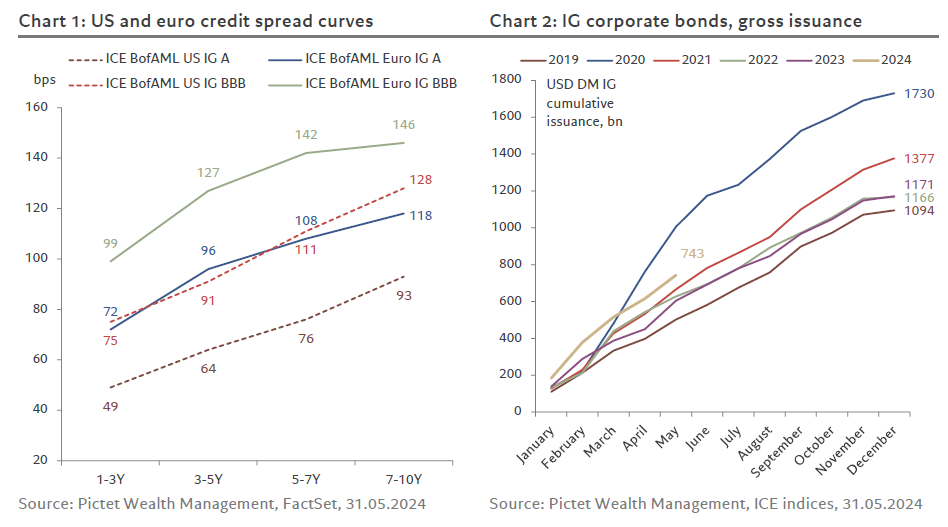

Additionally, demand for quality corporate bonds has been strong as investors seek to lock in elevated yields from quality issuers as central banks pivoted from rate hikes to talk of rate cuts last December. Moreover, while sovereign yield curves are inverted, corporate bond yield curves are flat thanks to steep credit spread curves, ensuring that investors are compensated for the duration risk they take. For exam- ple, US IG yields hover around 5.5% across maturities and euro IG ones around 4%, with credit spreads below 100 bps for short-dated maturities both in US and euro IG, but above 100 bps for mid-to-longer dated issues (according to ICE indices, chart 1).

IG companies have taken advantage of investors’ appetite for quality debt, and the ensuing spread tightening, to issue. Gross developed market (DM) IG issuance came to USD743 bn in the first five months of 2024, the highest level ever for a compara- ble time period (except in 2020, chart 2). Although the strength of new issuance has contributed to the afore-mentioned fall in the interest coverage ratios of IG compa- nies, it has also helped push back the ‘maturity wall’ that IG companies were facing into 2025 and beyond.