Below you will find a new commentary by Frederik Ducrozet, Head of Macroeconomic Research, at Pictet Wealth Management, ahead of this Thursday’s ECB meeting.

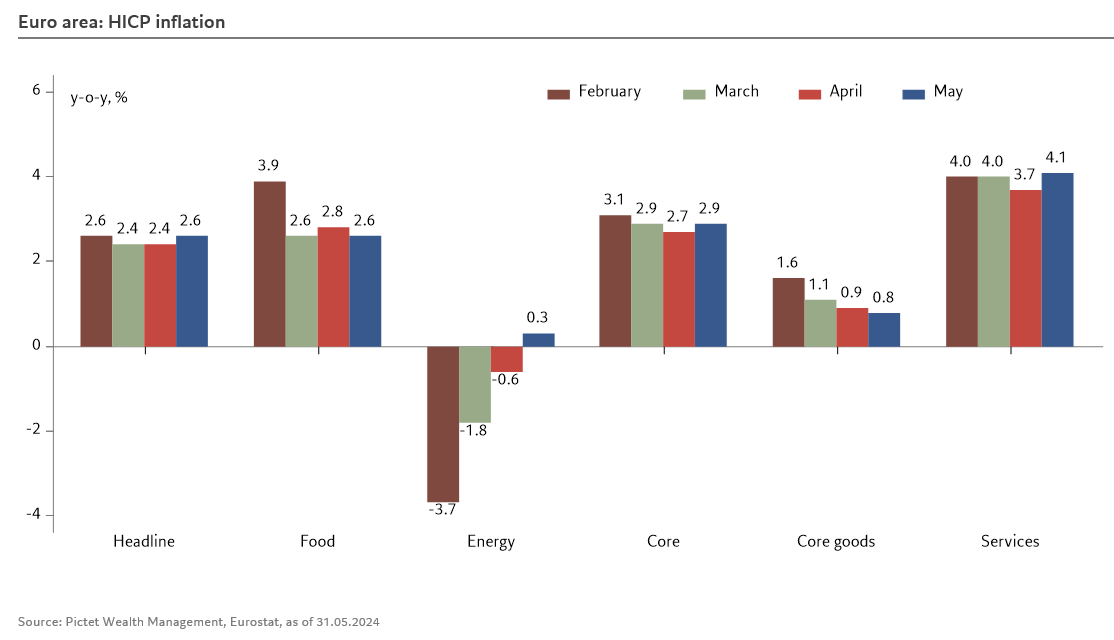

- Inflation surprised the consensus to the upside today, with the headline HICP figure accelerating more than expected to 2.6% y/y in May. Most importantly, core inflation rose to 2.9%, two tenths above consensus expectations, driven by services inflation, which is back above 4% after a temporary dip in April, while core goods inflation has eased again (+0.8%). Energy inflation is back in positive territory (+0.3%), while food inflation fell slightly (+2.6%). This surprise comes on top of last week’s acceleration in negotiated wages in Q1, a pick-up that we believe to be temporary.

- Despite a contrasting data flow, the ECB is all but certain to cut rates at its meeting on 6 June, a move that has long been telegraphed to the markets and is likely to be unanimously approved by the Governing Council. Moreover, Christine Lagarde made it clear back in April that the Governing Council was prepared for some jolts in the disinflation process.

- Next week the focus will be elsewhere, on what happens after June. First of all, markets will be looking to see if the meeting provides any clues about future interest rate decisions. The most likely outcome is that the Governing Council will stick to its current approach of taking decisions based on incoming data, one meeting at a time. Another option would be to make an explicit reference to future interest rate decisions being taken on a quarterly basis, supported by updated staff macroeconomic projections. This view seems to be gaining ground among the hawks, and was explicitly supported by the influential Dutch governor Klaas Knot in a speech this week. Such an option would reassure the current market pricing of future ECB interest rates (a pricing that Knot did not push back on), and keep the staff projections – which in turn use market pricing as an input – consistent with inflation returning to target by next year. This may sound like a circular argument, but it would be consistent with the heightened uncertainty around the inflation outlook and thus the central bank’s extreme data dependency.

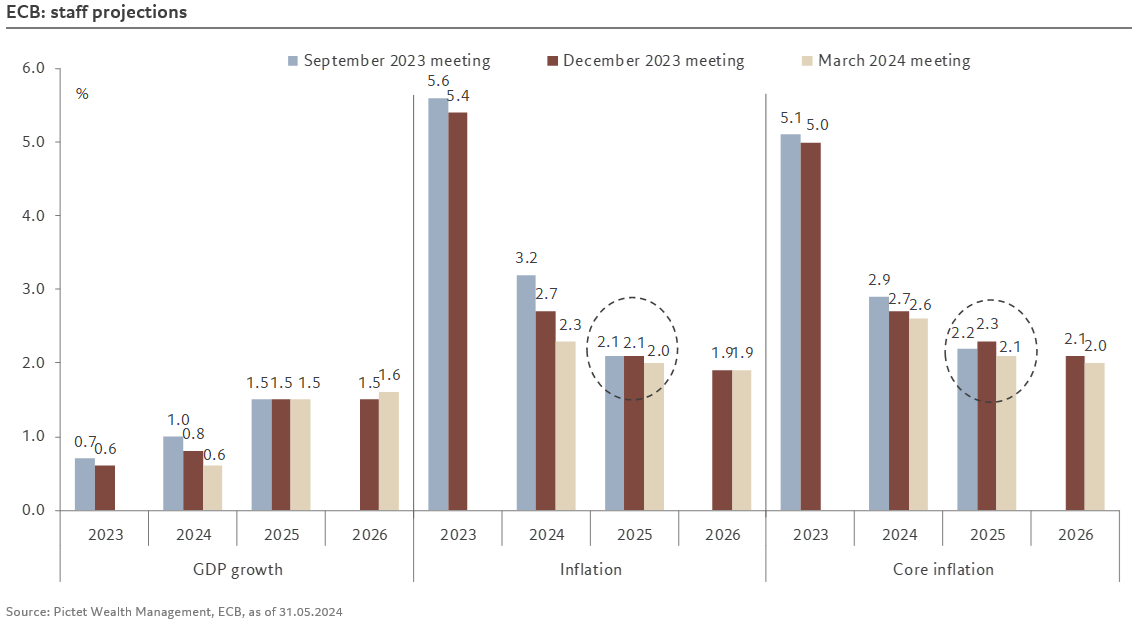

- Second, markets will focus on the updated staff projections. Changes in the technical assumptions since March argue for marginal changes, but they should be on the hawkish side. GDP growth and inflation projections for 2024 should be revised slightly higher, reflecting recent developments.