Please find below a new comment from Frederik Ducrozet, Head of Macroeconomic Research, at Pictet Wealth Management, on today’s ECB meeting:

ECB: one step at a time

- As widely expected, the ECB cut its key rates by 25 basis points, bringing the deposit facility rate down to 3.75%. Looking ahead, the Governing Council will stick to its meeting-by-meeting approach for future rate decisions, as the central bank needs more data to “continuously confirm the disinflationary path”, according to Christine Lagarde. It was also confirmed that the reinvestment of the principal payments of the PEPP will be reduced by half, as planned, from July.

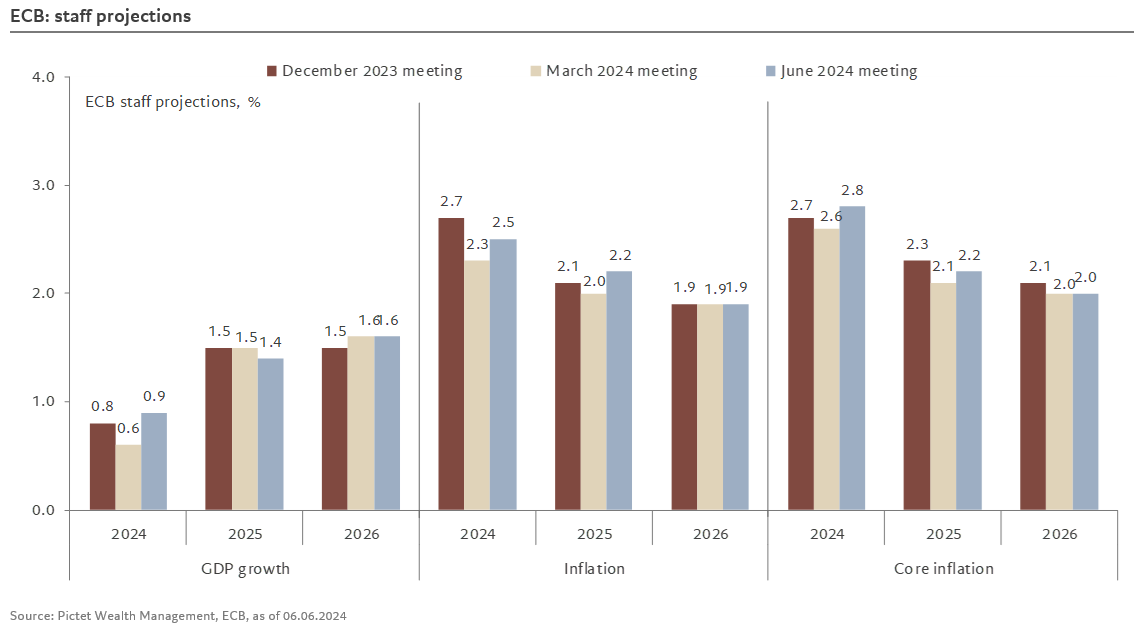

- The upward revisions to the staff’s inflation projections for 2024 and 2025 for both headline and core were not enough to prevent a cut that had already been telegraphed to the markets. Headline inflation was revised up 2/10ths to 2.5% in 2024 and 2.2% in 2025. Core inflation was revised up 2/10ths to 2.8% in 2024 and 1/10th to 2.2% in 2025, reflecting a combination of factors including higher expected GDP and labour cost growth in 2024. It is also very likely that the bulk of these revisions are due to a limited number of countries, including Germany, which should be verifiable soon with the publication of the national banks’ projections.

- Confidence that the disinflation process remains on track seems to have been the main motivation for the cut, despite higher inflation projections. The fact that the updated core inflation projection for 2024 remained unchanged despite a higher-than-expected print in May (which was not published at the time of the projection) certainly played a role. Most importantly, however, the staff’s quarterly inflation projection still sees inflation converging to 2% in 2025 by the end of the year and, as Christine Lagarde pointed out, the remarkable stability of the staff’s projections on this horizon over the last few rounds of projections has strengthened the Governing Council’s confidence that, despite the bumps, inflation will converge to the objective over the medium term. Last but not least, Christine Lagarde recalled that despite the upside surprise in negotiated wage growth in Q1 2024, the surprise was mainly led by Germany. Furthermore, the Governing Council still saw tentative signs of stabilisation, while the ECB’s wage tracker was pointing to declining wages going forward.

- Looking ahead, recent sticky services inflation and wage growth, combined with the staff’s higher inflation projections, close the door to another rate cut in July, in line with our scenario. Barring any major surprises in incoming data, we maintain our view that the ECB will resume its cuts at the September meeting. In fact, one could argue that the higher inflation projections lower the bar for a September cut, as the staff forecast is now more likely to be surprised to the downside by incoming data, especially given the fading of past Easter effects and German one-offs on price dynamics.