Please find below a new comment from Nadia Gharbi, Senior Economist, at Pictet Wealth Management, ahead of this Thursday’s ECB meeting

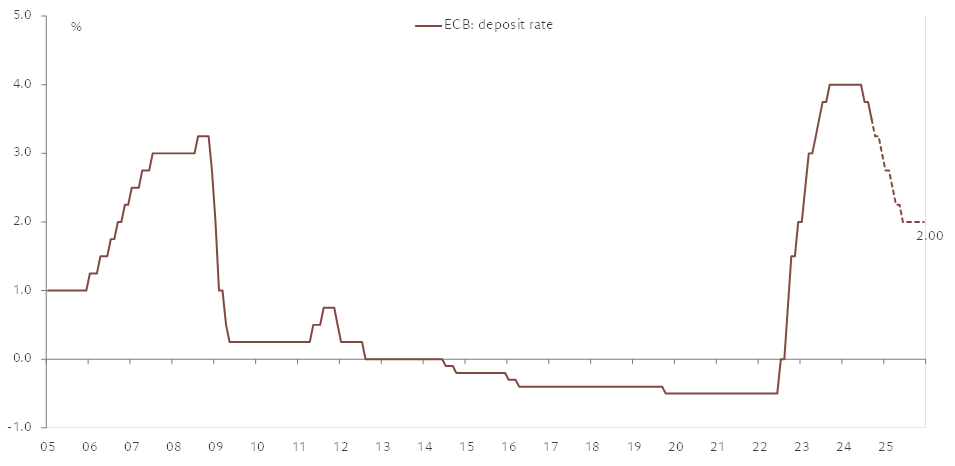

- With September data pointing to weaker growth and inflation dynamics than the ECB staff projections, a consensus seems to have emerged within the Governing Council that a more rapid pace of rate cuts was warranted. We thus expect the Governing Council (GC) to cut its key interest rates by 25 basis points on 17 October, bringing the deposit facility rate (DFR) down to 3.25%. The October rate cut will thus be the first back-to-back cut (the ECB also cut rates in September) and is likely to signal a pivot to a faster rate cut cycle, although ECB President Christine Lagarde is likely to insist that the bank will stick to a “meeting by meeting” and “data-dependent” approach.

- Looking ahead, we expect the ECB to accelerate the easing of financing conditions and bring forward convergence to neutral (which we think is around 2%), with 25bp cuts at each GC meeting from now until June 2025, as we now see a higher probability that the staff will revise its growth and inflation forecasts downwards. This implies another 25bp cut in December and a total of 100bp cuts in H1 2025.

- We also see a risk that the ECB will have to cut rates even faster than we now forecast and possibly bring the DFR below its neutral level.The probability of the staff’s inflation projections falling below target over the medium term has increased significantly, and the dynamics of growth, the labour market and inflation expectations will need to be monitored closely in this regard. The GC’s communication on its assessment of the neutral interest rate will also be crucial: a move towards a lower level would justify a more rapid reduction.