You will find below a commentary by Frederik Ducrozet, Head of Macroeconomic Research at Pictet Wealth Management, ahead of the ECB meeting next Thursday (7 March).

- The timing of the first ECB rate cut is important (we stick to June), but eventually the debate will turn to the pace and magnitude of policy easing beyond summer.

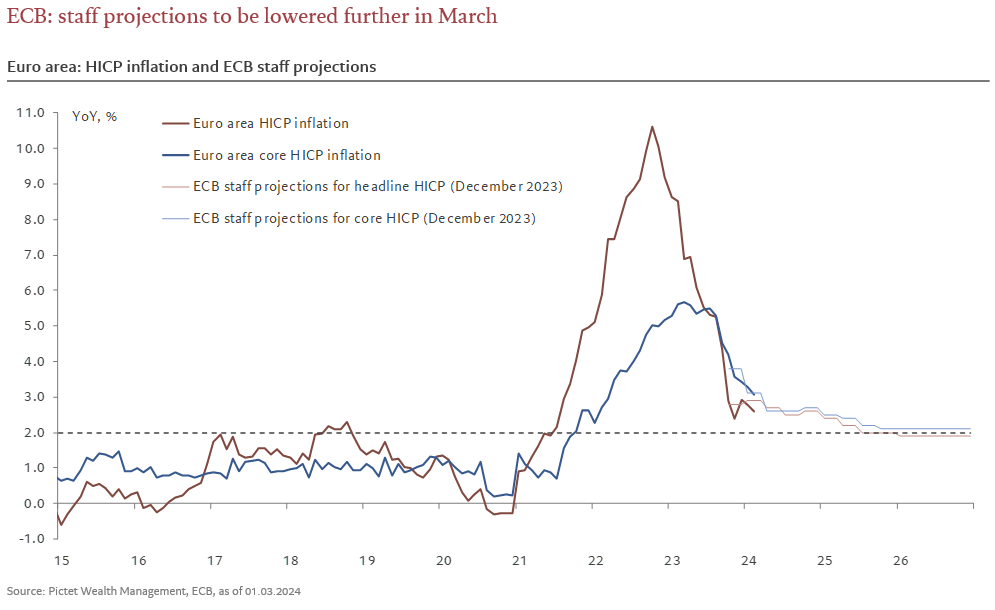

- This week the Governing Council (GC) will reassess the inflation outlook based on the updated macroeconomic projections from the staff as well as the latest HICP prints. We expect a neutral policy stance and balanced communication, acknowledging the continued progress on inflation but avoiding a premature declaration of victory.

- On the one hand, mixed hard data should be consistent with a downward revision to the staff projection for 2024 real GDP growth, closer to our own forecast (+0.6%). The sharp decline in electricity and gas prices since December will likely drive a downward revision to headline HICP inflation throughout the forecast horizon, mitigating the downside risks to growth beyond this year. The net result of slightly weaker growth and recent upside surprises in core services inflation is unclear, but on balance we think that staff projections for core inflation should be revised slightly lower (by 10bp on average), all the way to 2% by 2026 – a dovish signal in itself. On the other hand, wage growth remains elevated with little sign of a rapid turnaround yet, fueling the stickiness in services inflation.

- Either way, it will take some time before the ECB is fully convinced that Lagarde’s three inflation criteria are fully met, ie. that the inflation outlook is consistent with a sustained return to the 2% target over the medium-term. We stick to our view that June is the most likely date for a first rate cut, with a lower risk of an earlier move in April than we estimated at the start of the year.

- Looking ahead, we expect the ECB to ease monetary policy in a gradual fashion, cutting rates by a cumulative 100bp in 2024 and bringing the deposit facility rate to 3% in December. In particular, the ECB may choose to leave policy rates unchanged in July before resuming its easing cycle in September. However, faster policy transmission and a lower neutral rate than in the US, along with a more important role of demand factors driving the inflation outlook, should be consistent with a more sustained ECB easing cycle than in the US eventually.

- Last but not least, the ECB’s review of its operational monetary framework may be discussed this week, including the timing of its conclusions (expected by “late Spring”), but we are unlikely to get much details at this point. The review is likely to lead to some important technical changes, including a floor system to steer money market rates and possibly a modest increase in reserve requirements, although the macroeconomic consequences of these changes are likely to remain limited.