China’s incipient recovery, primed by rounds of stimulus, is adding to emerging markets’ positive momentum, compounding the effects of falling global interest rates and trade normalisation.

Patrick Zweifel, Chief Economist Pictet Asset Management.

In late September, China’s economy had deteriorated sufficiently – consumption and investment were sliding and deflation was becoming entrenched – to force Beijing into launching a major round of monetary stimulus.

Helping Chinese authorities was the US Federal Reserve’s earlier rate cut, which gave the Peoples Bank of China (PBoC) the latitude to reduce its own rates without risking an excessive depreciation of the yuan. Total measures, including rate cuts and equity market support, amounted to some 1.5 per cent of GDP. A tax cutting plan is expected to follow by the end of the year – likely calibrated to the outcome of the US election – worth an additional 1.6 per cent of GDP. Together they should ensure the economy meets Beijing’s 5 per cent growth target.

Investor confidence duly soared. In a single session, Chinese stocks jumped 8.5 per cent, their biggest one-day gain since 2008. Since its January low, the total return in dollars of Chinese equities has been some 43 per cent.

China’s return to target growth is good news for other emerging market economies. More generally, it stimulates global investors’ appetite for risk. At the same time, rising Chinese consumption and investment will increase demand for imports – regional economies are closely tied to China – for foreign travel and for outward direct investment by Chinese companies.

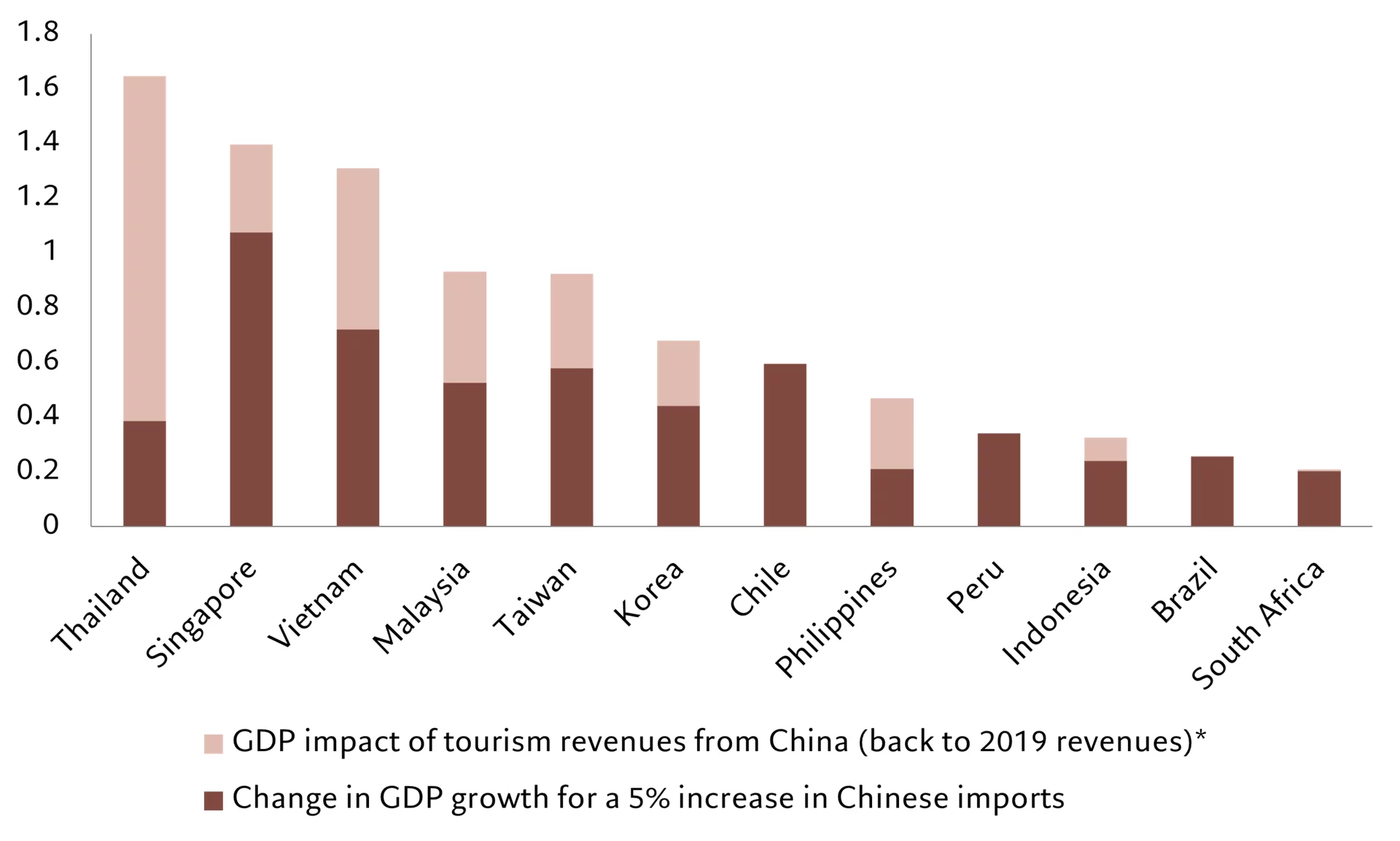

Fig. 1 – China impact

Impact of an increase in Chinse imports and tourism, % of GDP

*Assuming that Chinese tourism returns to its 2019 level (currently less than 60%). Source: Pictet Asset Management, CEIC, Refinitiv. Data as at 01.10.2024.

We think a rebound in domestic demand should see Chinese import growth return to its pre-pandemic average of 6 per cent – some 5 percentage points above current rates. Outward Chinese tourism is still 40 per cent below its 2019 level.

Combined recovery in both would be particularly significant for ASEAN economies in particular, led by Thailand – where Chinese trade and tourism accounts for 1.6 per cent of GDP – followed by North-East Asia, notably Taiwan and Korea, and to a lesser extent Latin America, where Chile would be the main beneficiary (see Fig. 1).

China’s direct investment abroad, which is increasing structurally in response to its shrinking population and trade tensions with the US, is largely dependent on economic growth and re-investable corporate profits. Cambodia and Laos receive the largest share of these investments in relation to their GDP – more than 3 per cent and 7 per cent respectively – while among the larger emerging countries, Vietnam stands to gain most.

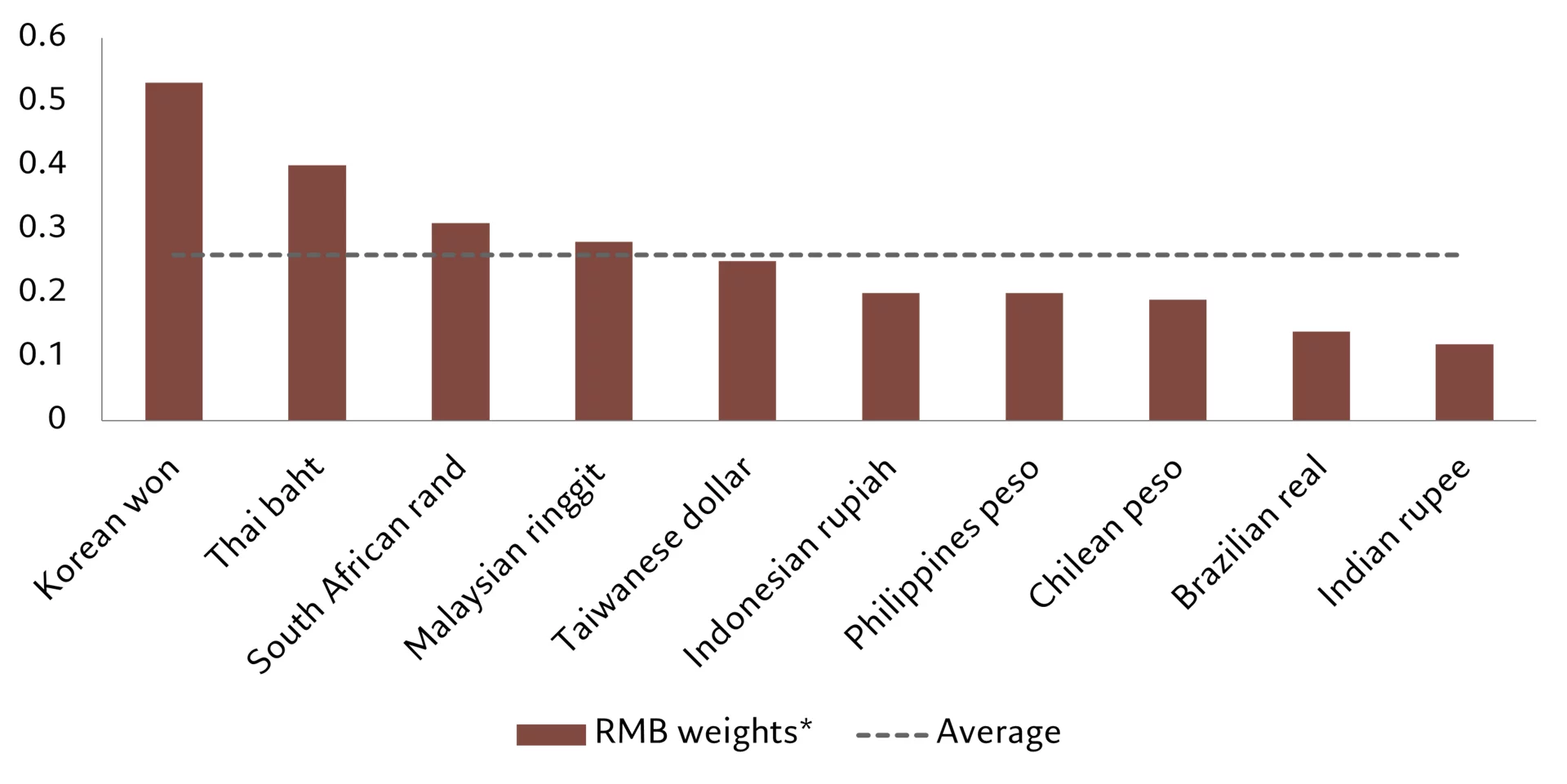

Fig. 2 – FX effects

Main emerging market currencies’ sensitivity to renminbi

*2-step Frankel-Wei rolling regression (average with CAD, NZD and CHF as numeraire), indicates average move of currency for a 1% move in renminbi. Source: Pictet Asset Management, CEIC, Refinitiv. Data as at 01.01.2024.

The renminbi has also gained strength from China’s stimulus programme, on expectations of stronger growth and on a narrowing rate differential between China and the US – the PBoC is expected to cut less than the Fed. Currencies closely linked to the renminbi – notably the Korean won, the Thai baht and the South African rand – are also likely to benefit (see Fig. 2). It could further push the integration of the region towards a renminbi zone.

The average sensitivity of Asian currencies to movements in the renminbi was zero as recently as 2009; by mid-2024, it had risen to over 20 per cent. In other words, a 10 per cent rise in the renminbi, which had no impact on Asian currencies 15 years ago, now causes an average rise of 2 per cent, and more than 5 per cent for the most renminbi-sensitive currency, the Korean won.

With emerging market economies already set to outgrow the developed world, China’s stimulus could further widen that differential. That should help emerging market assets.

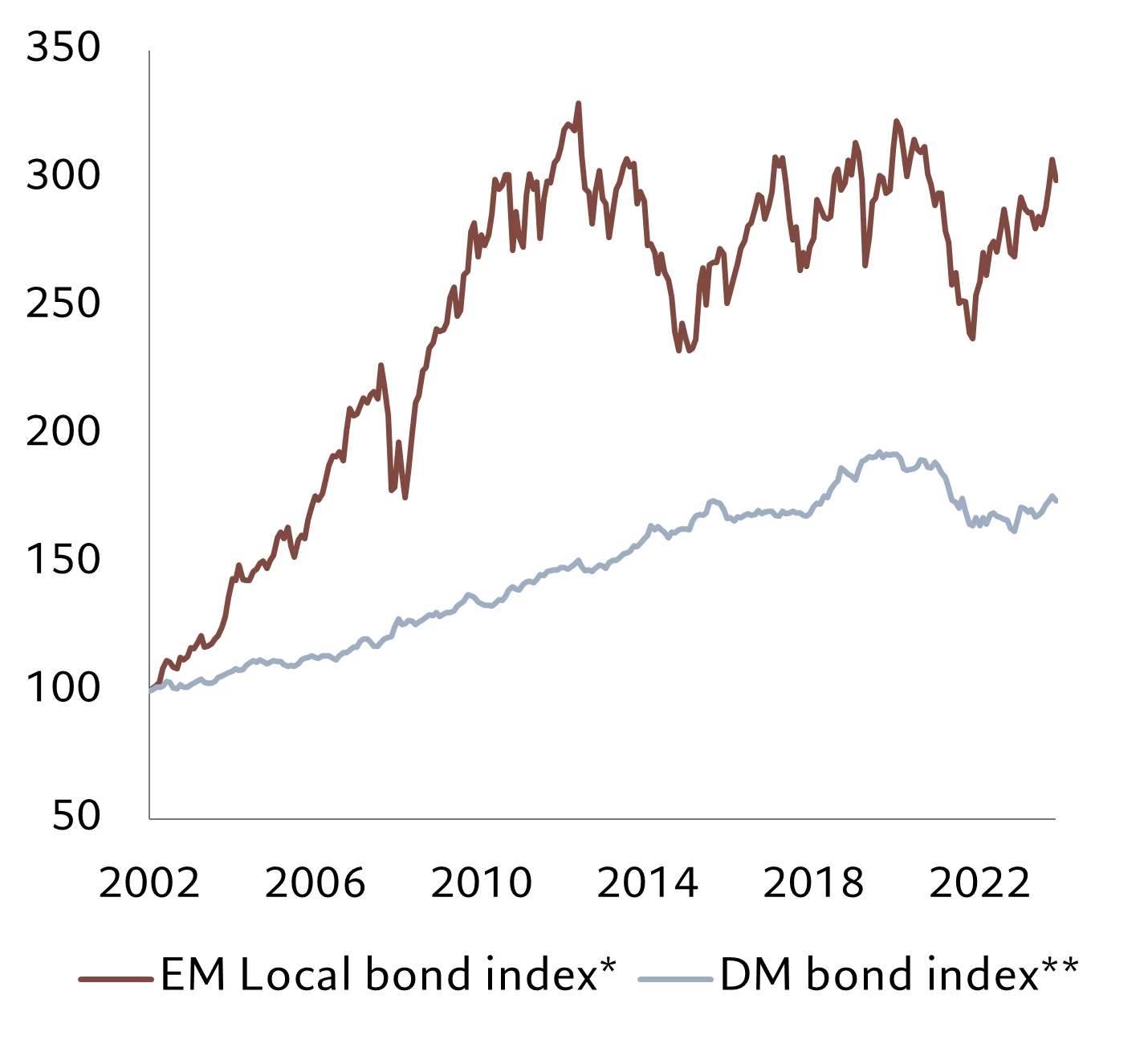

Earlier this year, emerging equity and bond markets performed poorly. But lately they’ve started to recover. So while emerging equities are still underperforming developed markets by 4 per cent, they’re up 5 per cent from recent lows. Meanwhile, emerging bonds have gained 4 per cent from lows and are now outperforming their developed counterparts by 0.7 per cent (see Fig. 3).

Fig. 3 – Emerging gap

Emerging and developed bond markets, rebased to 01.12.2002 = 100

*JPM global diversified (EM global sovereign in local currency). **JPM GBI (DM global sovereign). Source: Pictet Asset Management, CEIC, Refinitiv, Bloomberg. Data covering period 01.12.2002 to 01.10.2024.

What’s more, China’s stimulus adds to the already positive effects on emerging economies of US monetary easing – as well as the gradual normalisation of world trade and the stabilisation of the dollar.

The Fed is a major contributor to the easing of global monetary conditions. Its rate cut supports emerging markets through three main channels. First, it reduces the risk of a severe slowdown in the US economy and thus supports sentiment more generally. Second, it allows emerging market central banks to cut their own interest rates without fear of depreciating their currencies – which would have inflationary consequences. And third, and most crucially, it lowers the cost of servicing dollar-denominated debt. Given that both sovereign and corporate borrowers in emerging markets often borrow in dollars, that reduces their vulnerability to default and frees capital for more productive investment in both the public and private sectors. A weaker dollar can also push up commodity prices, which benefits producer countries.

The overall performance of emerging market assets has, until recently, been driven by emerging countries with strong manufacturing bases and that are creditors to the rest of the world. But recent developments in China and the US make it possible for emerging debtor countries to outperform as well – albeit depending on a recovery in commodity prices and the result of the US election.