Below you will find a new comment from Xiao Cui, Senior Economist, at Pictet Wealth Management, ahead of next Wednesday’s Fed meeting :

A few days before the first cut of the Fed easing cycle, markets are pricing in -36bps for next week, essentially split on whether the Fed will go with a traditional 25bps rate reduction, or a bigger 50 bps cut (Nikileaks suggest the decision is a close call). This is unusual and further highlights the uncertainty around the speed and depth of the easing cycle.

We expect the FOMC to start with a 25bps rate cut and rate projections to indicate a gradual pace of easing consistent with policy normalization, not labor market rescue. We expect median rate projections to show 75bps of cuts this year, followed by 125bps in 2025, both higher than markets pricing. We expect the median economic projections to show an increase in unemployment and a decline in inflation for this year, and the contour of the projections to remain consistent with a soft landing. The risk distributions will likely skew dovish for growth and labor markets. Although a 25bps cut could potentially be seen as a policy error or evidence that the Fed is falling further behind the curve, we expect Powell to be dovish and open-minded to the possibility of larger cuts, stressing the flexibility for more aggressive easing if the labor market weakens. An extremely weak retail sales report or a major financial shock ahead of the meeting will make the Fed cut 50bps.

The decision on 25 vs. 50bps hinges on the FOMC’s appetite to ease aggressively before labor-market stress materializes, and there are good reasons to think the Fed should start big and get back to neutral rapidly. However, in past cycles, large cuts have typically coincided with significant stress in labor markets or financial conditions. Even though Fed leadership has not ruled out a 50bps reduction, we don’t think the committee consensus is there yet given the current data.

If we are wrong and the Fed decides to start with a 50bps cut, this would likely encourage expectations that the Fed will go to neutral very quickly. It would signal that the Fed is 1) willing to be truly pre-emptive and 2) sees higher risks of a sharper labor market slowdown than we do. In that case, another 50bps rate cut in November and/or December as the base case would seem reasonable.

The dot plot, economic projections, and Powell’s presser will all be key, but we expect the labor market data to ultimately dictate the shape of the cycle. If evidence of weaker labor demand or increases in layoffs emerge, FOMC wouldn’t hesitate to react forcefully.

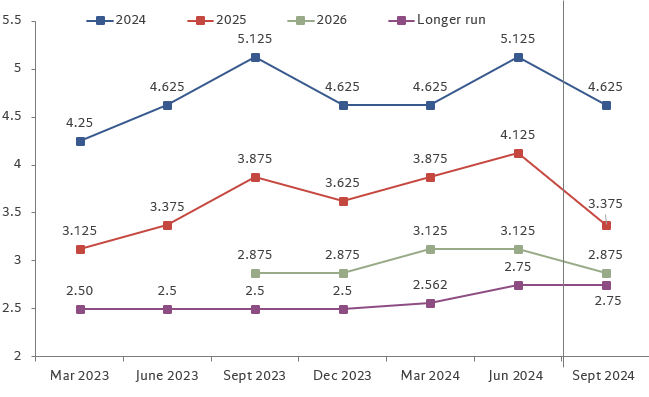

Specifically, we expect the median dot to show 75bps this year and 125bps of easing in 2025. It’s possible that some officials have already penciled in 100bps or 125bps of cuts for this year. If the Fed decides to go with 50bps already in September, we’d expect the dot plot to show a median of 125bps of cuts this year. The 2026 and 2027 dots will converge to the Fed’s neutral projection, which we expect to stay at 2.75%.

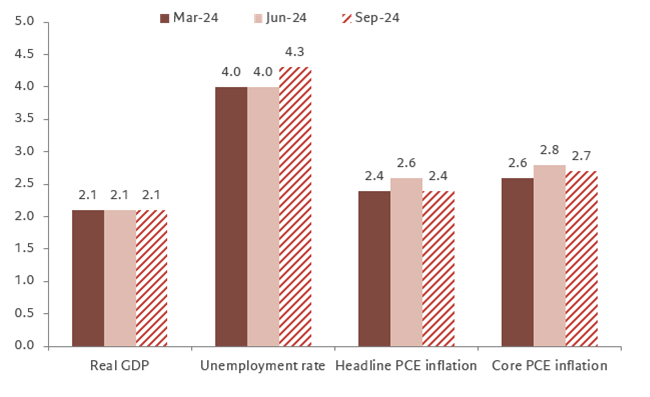

We expect the unemployment rate forecast for this year to rise to 4.3% from 4.0%. Core inflation forecast should move lower to 2.7% (potentially even 2.6%) from 2.8% for core PCE. We don’t expect major changes to real GDP or to longer-term estimates.

The policy statement will likely note the recent rise in unemployment and the encouraging news on the inflation front. We don’t expect the word “gradual” in the forward guidance regarding the pace of future cuts. Instead, the Fed will likely retain optionality and notes that further reductions will depend on data and the balance of risks.

We don’t expect any announcement on QT. QT has tapered and remains a process running in the background. Even if the Fed cuts 50bps next week, it does not seem likely that QT would stop. We expect the decision to end QT to be a function of reserve ampleness and money market stress, unless there is a significant economic deterioration.

Dot plot with our forecast for Sept – median interest rate projection

Median economic projections for 2024, with our forecast