Please find below a comment from Nadia Gharbi, Senior Economist at Pictet Wealth Management.

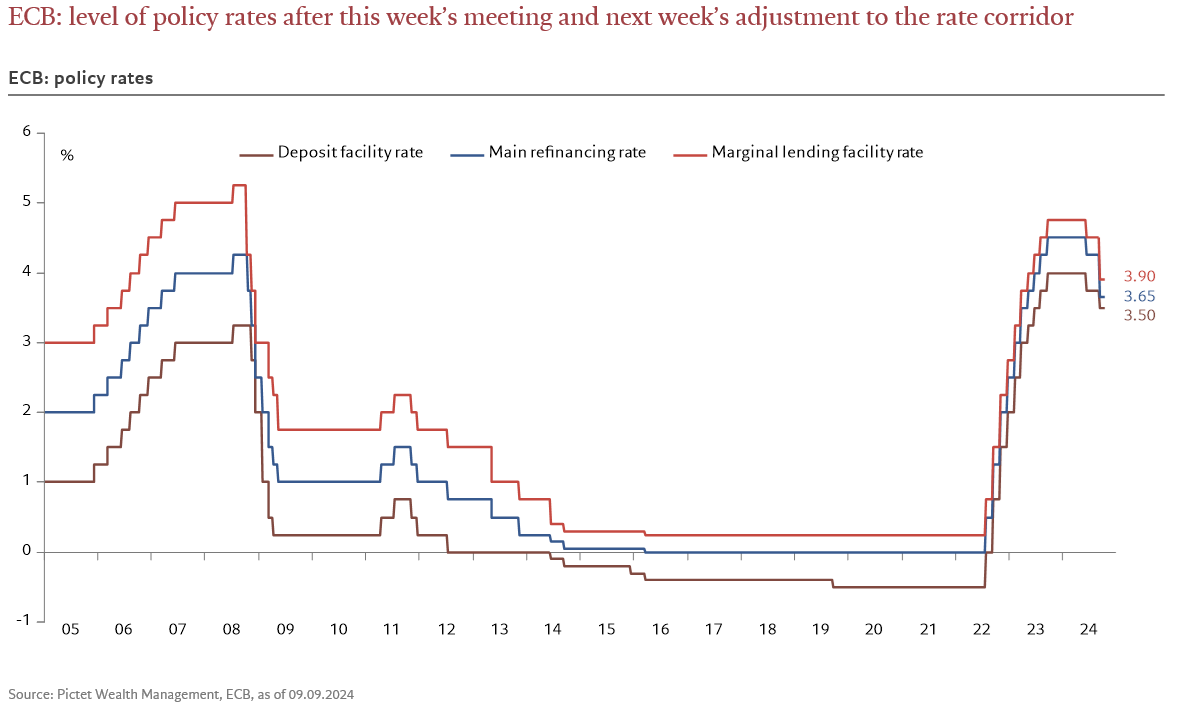

- We expect the European Central Bank (ECB) to cut its deposit facility rate (DFR) by 25bp to 3.50% on September 12. A cut is widely expected, so the focus will be on what the ECB says about the next steps “in the dialling back of its restrictive policy stance”. While the direction of rates remains downwards, ECB president Christine Lagarde is unlikely to give an unequivocal signal about the size and timing of the next move.

- The new ECB staff projections are likely to be revised slightly, but without major implications for the policy stance. Activity data have been weaker than expected in the June staff projections. Q2 GDP was revised down to 0.2% q-o-q (vs. 0.4% projected by the ECB), with very weak details in the national accounts. Soft data so far point to subdued momentum in Q3, with growth expected to be close to 0.1-0.2% q-o-q. Meanwhile, inflation data have been mixed. On the one hand, core inflation has been more resilient than expected, reflecting persistently high services inflation. On the other hand, measures of labour cost growth slowed more than expected in Q2, including the ECB’s measure of negotiated wages (down from 4.7% y-o-y in Q1 to 3.6% in Q2) and compensation per employee (down from 4.8% in Q1 to 4.3% in Q2). Against this backdrop, domestic price pressures, as measured by the growth of the GDP deflator, have eased faster than expected, also supported by the stagnation of corporate profits over a year. Overall, we expect the ECB staff to revise its growth forecasts slightly lower (by around 0.1pp for 2024 and 2025) and its core inflation forecasts slightly higher (by 0.1pp for 2024 and 2025), mainly due to a higher starting point. Importantly, these revisions should not affect the ECB staff’s projection that inflation will reach the central bank’s 2% target around the fourth quarter of 2025. For the record, Christine Lagarde highlighted the stability of this projection as a factor behind the June rate cut, despite the upward revision of the 2025 inflation forecast at that time.

- The Q&A session is likely to focus on what the ECB would do in the event of a weaker US/global growth outlook and a more aggressive Fed. While Lagarde is likely to hold back and mention that the ECB is not dependent on the Fed, a larger than expected cut by the Fed could increase pressure on the ECB and could make the October meeting live.

- In addition to this week’s cut, on 18 September the ECB will also reduce the spread between the main refinancing operation (MRO) rate and the DFR to 15bp from 50bp today. The spread between the marginal lending facility (MLF) rate and the MRO rate will remain unchanged at 25 bps. The decision is a key measure of the changes to the operational framework announced in March. In total, the ECB will have “cut” the MRO rate by 60 pbs in one week. The rationale behind the decision on the MRO-DFR corridor is to create the conditions for increased participation by banks in the ECB’s conventional refinancing operations (7-day MROs and 90-day LTROs) at a time when the last TLTROs are due to be repaid in December. For the record, the outstanding liquidity provided through TLTROs has fallen from EUR 2,220 billion during the pandemic to EUR 85 billion last week.

- Apart from the rate decision, we do not expect any news on the balance sheet front. The QT is likely to continue as the ECB will no longer reinvest principal payments from maturing securities in the APP and will only continue to reinvest half of the principal payments from maturing securities purchased under the PEPP until the end of the year (before the end of PEPP reinvestments in 2025).

- All in all, we expect a 25-bps cut in the deposit rate this week, followed by another one in December. The risks are tilted towards further easing in the coming months. A weaker US/world growth outlook and a bigger-than-expected Fed cut could increase pressure on the ECB to do more than is currently priced in.